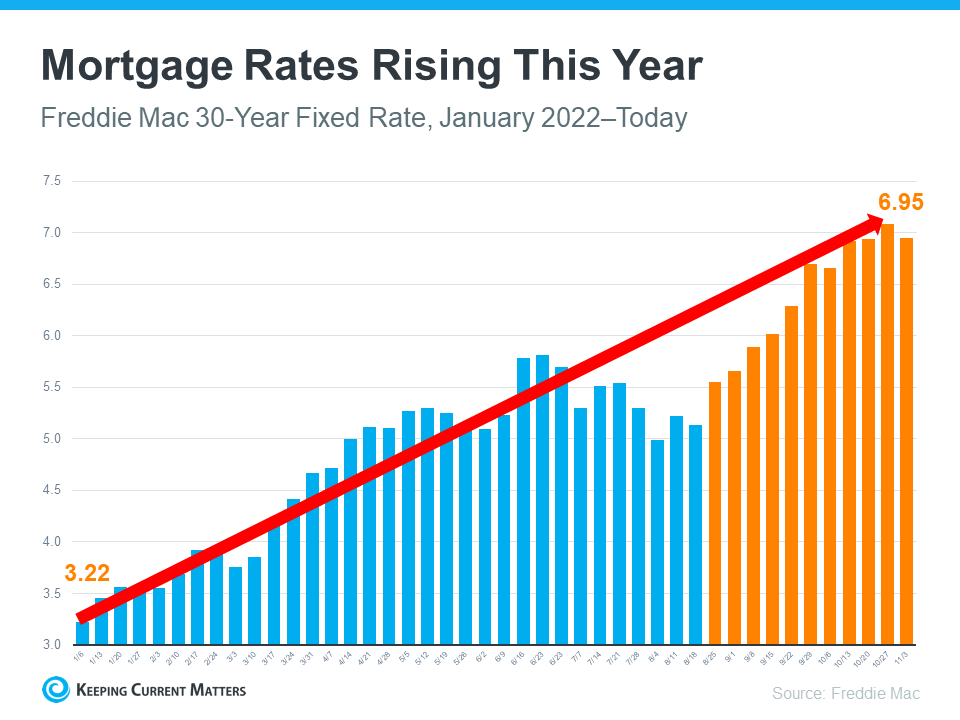

There’s no denying mortgage rates are higher now than they were last year. And if you’re thinking about buying a home, this may be top of mind for you. That’s because those higher rates impact how much it costs to borrow money for your home loan. As you set out to make a purchase this winter, you’ll need to be strategic so you can find a home that meets your needs and budget.

Danielle Hale, Chief Economist at realtor.com, explains:

“The key to making a good decision in this challenging housing market is to be laser focused on what you need now and in the years ahead, . . . Another key point is to avoid stretching your budget, as tempting as it may be given the diminished purchasing power.”

In other words, it’s important to be mindful of what’s a necessity and what’s a nice-to-have when searching for a home. And the best way to understand this is to put together a list of desired features for your home search.

The first step? Get pre-approved for a mortgage. Pre-approval helps you better understand what you can borrow for your home loan, and that plays an important role in how you’ll craft your list. After all, you don’t want to fall in love with a home that’s out of reach. Once you have a good grasp of your budget, you can begin to list (and prioritize) all the features of a home you would like.

Here’s a great way to think about them before you begin:

- Must-Haves – If a house doesn’t have these features, it won’t work for you and your lifestyle (examples: distance from work or loved ones, number of bedrooms/bathrooms, etc.).

- Nice-To-Haves – These are features that you’d love to have but can live without. Nice-To-Haves aren’t dealbreakers, but if you find a home that hits all the must-haves and some of the these, it’s a contender (examples: a second home office, a garage, etc.).

- Dream State – This is where you can really think big. Again, these aren’t features you’ll need, but if you find a home in your budget that has all the must-haves, most of the nice-to-haves, and any of these, it’s a clear winner (examples: farmhouse sink, multiple walk-in closets, etc.).

Finally, once you’ve created your list and categorized it in a way that works for you, discuss it with your real estate advisor. They’ll be able to help you refine the list further, coach you through the best way to stick to it, and find a home in your area that meets your needs.

Bottom Line

Putting together your list of necessary features for your next home might seem like a small task, but it’s a crucial first step on your homebuying journey today. If you’re ready to find a home that fits your needs, connect with a local real estate advisor.