Wednesday, September 28, 2016

Monday, September 26, 2016

Don't Underestimate the Importance of Using an Agent When Selling Your Home

When a homeowner decides to sell their house, they obviously want the best possible price with the least amount of hassles. However, for the vast majority of sellers, the most important result is to actually get the home sold. In order to accomplish all three goals, a seller should realize the importance of using a real estate professional. We realize that technology has changed the purchaser's behavior during the home buying process. For the past three years, 92% of all buyers have used the internet in their home search according to the National Association of Realtors' most recent Profile of Home Buyers & Sellers. However, the report also revealed that 95% percent of buyers that used the internet when searching for a home purchased their home through either a real estate agent/broker or from a builder or builder's agent.Only 2% purchased their home directly from a seller whom the buyer didn't know. Buyers search for a home online, but then depend on an agent to find the actual home they will buy (53%), to negotiate the terms of the sale & price (48%), or to help understand the process (60%). The plethora of information now available has resulted in an increase in the percentage of buyers that reach out to real estate professionals to "connect the dots." This is obvious, as the percentage of overall buyers who used an agent to buy their home has steadily increased from 69% in 2001. When a homeowner decides to sell their house, they obviously want the best possible price with the least amount of hassles. However, for the vast majority of sellers, the most important result is to actually get the home sold. In order to accomplish all three goals, a seller should realize the importance of using a real estate professional. We realize that technology has changed the purchaser's behavior during the home buying process. For the past three years, 92% of all buyers have used the internet in their home search according to the National Association of Realtors' most recent Profile of Home Buyers & Sellers. However, the report also revealed that 95% percent of buyers that used the internet when searching for a home purchased their home through either a real estate agent/broker or from a builder or builder's agent.Only 2% purchased their home directly from a seller whom the buyer didn't know. Buyers search for a home online, but then depend on an agent to find the actual home they will buy (53%), to negotiate the terms of the sale & price (48%), or to help understand the process (60%). The plethora of information now available has resulted in an increase in the percentage of buyers that reach out to real estate professionals to "connect the dots." This is obvious, as the percentage of overall buyers who used an agent to buy their home has steadily increased from 69% in 2001.Bottom LineIf you are thinking of selling your home, don't underestimate the role a real estate professional can play in the process. |

Friday, September 23, 2016

Pending Home Sales Tick Up in July

WASHINGTON (August 31, 2016) — Pending home sales expanded in most of the country in July and reached their second highest reading in over a decade, according to the National Association of Realtors®. Only the Midwest saw a dip in contract activity last month.

The Pending Home Sales Index,* a forward-looking indicator based on contract signings, rose 1.3 percent to 111.3 in July from a downwardly revised 109.9 in June and is now 1.4 percent higher than July 2015 (109.8). The index is now at its second highest reading this year after April (115.0).

Lawrence Yun, NAR chief economist, says a sizable jump in the West lifted pending home sales higher in July. “Amidst tight inventory conditions that have lingered the entire summer, contract activity last month was able to pick up at least modestly in a majority of areas,” he said. “More home shoppers having success is good news for the housing market heading into the fall, but buyers still have few choices and little time before deciding to make an offer on a home available for sale. There’s little doubt there’d be more sales activity right now if there were more affordable listings on the market.”

Adds Yun, “The index in the West last month was the highest in over three years 1 largely because of stronger labor market conditions. If homebuilding increases in the region to tame price growth and alleviate the ongoing affordability concerns, the healthy rate of job gains should support more sales.”

Recent residential construction data shows that the size and costs of new homes has moved downward over the past year. According to Yun, this is an early indication that homebuilders are beginning to shift away from building larger, more expensive homes for the upper end of the market to focusing more on properties geared for buyers in the middle and lower price tiers.

“Realtors® in several high-cost areas have been saying for quite a while that there is robust demand for single-family starter homes and townhomes at an affordable price point for young buyers,” adds Yun. “The homeownership rate won’t move up from its over 50-year low 2without a meaningful boost from first-time buyers, whose participation has yet to noticeably increase so far this year despite mortgage rates near all-time lows 3.”

Existing-home sales this year are forecast to be around 5.38 million, a 2.8 percent increase from 2015 and the highest annual pace since 2006 (6.48 million). After accelerating to 6.8 percent a year ago, national median existing-home price growth is forecast to slightly moderate to around 4 percent.

Regional Breakdown

The PHSI in the Northeast moved up 0.8 percent to 96.8 in July, and is now 1.1 percent above a year ago. In the Midwest the index decreased 2.9 percent to 105.8 in July, and is now 1.1 percent lower than July 2015.

Pending home sales in the South inched higher (0.8 percent) to an index of 123.9 in July and are now 0.4 percent higher than last July. The index in the West surged 7.3 percent in July to 108.7, and is now 6.2 percent above a year ago.

The National Association of Realtors®, “The Voice for Real Estate,” is America’s largest trade association, representing 1.1 million members involved in all aspects of the residential and commercial real estate industries.

# # #

1 The PHSI in the West in July was the highest since June 2013.

2 According to the U.S. Census Bureau, the homeownership rate is currently at 62.9 percent, which is the lowest since 1965.

3 According to the Realtors® Confidence Index, sales to first-time buyers in 2016 have averaged 31 percent through July; they were 30 percent in 2015. NAR’s 2015 Profile of Home Buyers and Sellers, representing transactions purchased between July 2014 and June of 2015, found that first-time buyers were 32 percent, the lowest since 1987 (30 percent). The average share in the survey’s 34-year history is 39 percent.

* The Pending Home Sales Index is a leading indicator for the housing sector, based on pending sales of existing homes. A sale is listed as pending when the contract has been signed but the transaction has not closed, though the sale usually is finalized within one or two months of signing.

The index is based on a large national sample, typically representing about 20 percent of transactions for existing-home sales. In developing the model for the index, it was demonstrated that the level of monthly sales-contract activity parallels the level of closed existing-home sales in the following two months.

An index of 100 is equal to the average level of contract activity during 2001, which was the first year to be examined. By coincidence, the volume of existing-home sales in 2001 fell within the range of 5.0 to 5.5 million, which is considered normal for the current U.S. population.

NOTE: NAR’s third quarter Housing Opportunities and Market Experience (HOME) survey will be released September 14, Existing-Home Sales for August will be reported September 22, and the next Pending Home Sales Index will be September 29; all release times are 10:00 a.m. ET.

Wednesday, September 21, 2016

Mortgage Standards Easing TOO MUCH? NO!!

There is no doubt that getting a mortgage is easier today than it was right after the housing crash a decade ago. However, the easing of credit availability has led to some questioning of whether or not we are headed for another housing crisis. Let's put everything into the proper perspective.

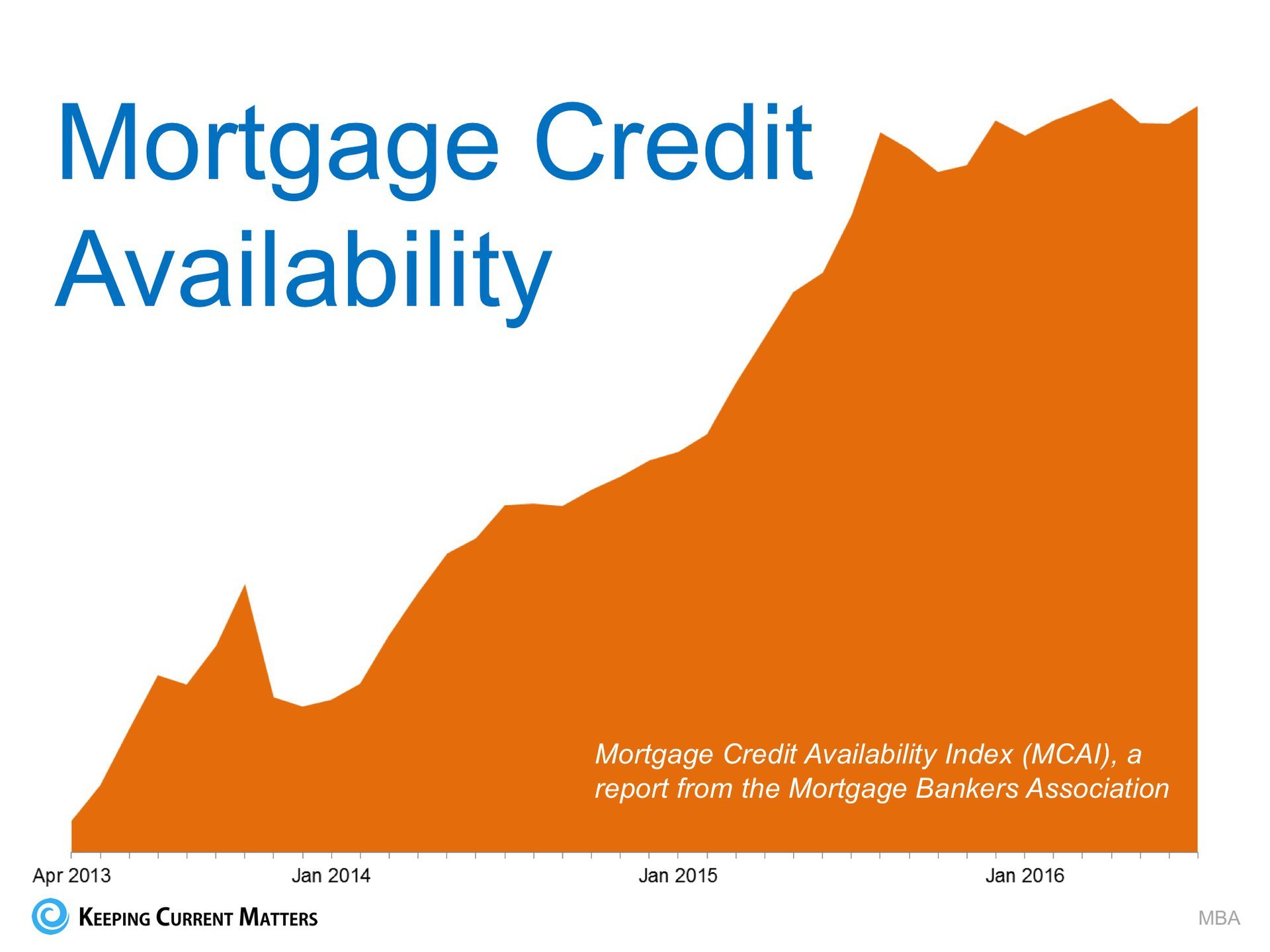

There is no doubt that getting a mortgage is easier today than it was right after the housing crash a decade ago. However, the easing of credit availability has led to some questioning of whether or not we are headed for another housing crisis. Let's put everything into the proper perspective.Mortgage Credit Availability Over the Last Three Years

Getting a home mortgage has definitely gotten easier over the last three years as evidenced by the Mortgage Credit Availability Index, issued by the Mortgage Bankers Association, in the following graph (the higher the index, the easier it is to get a mortgage): However, if we look further back at the index we see quite a different story.

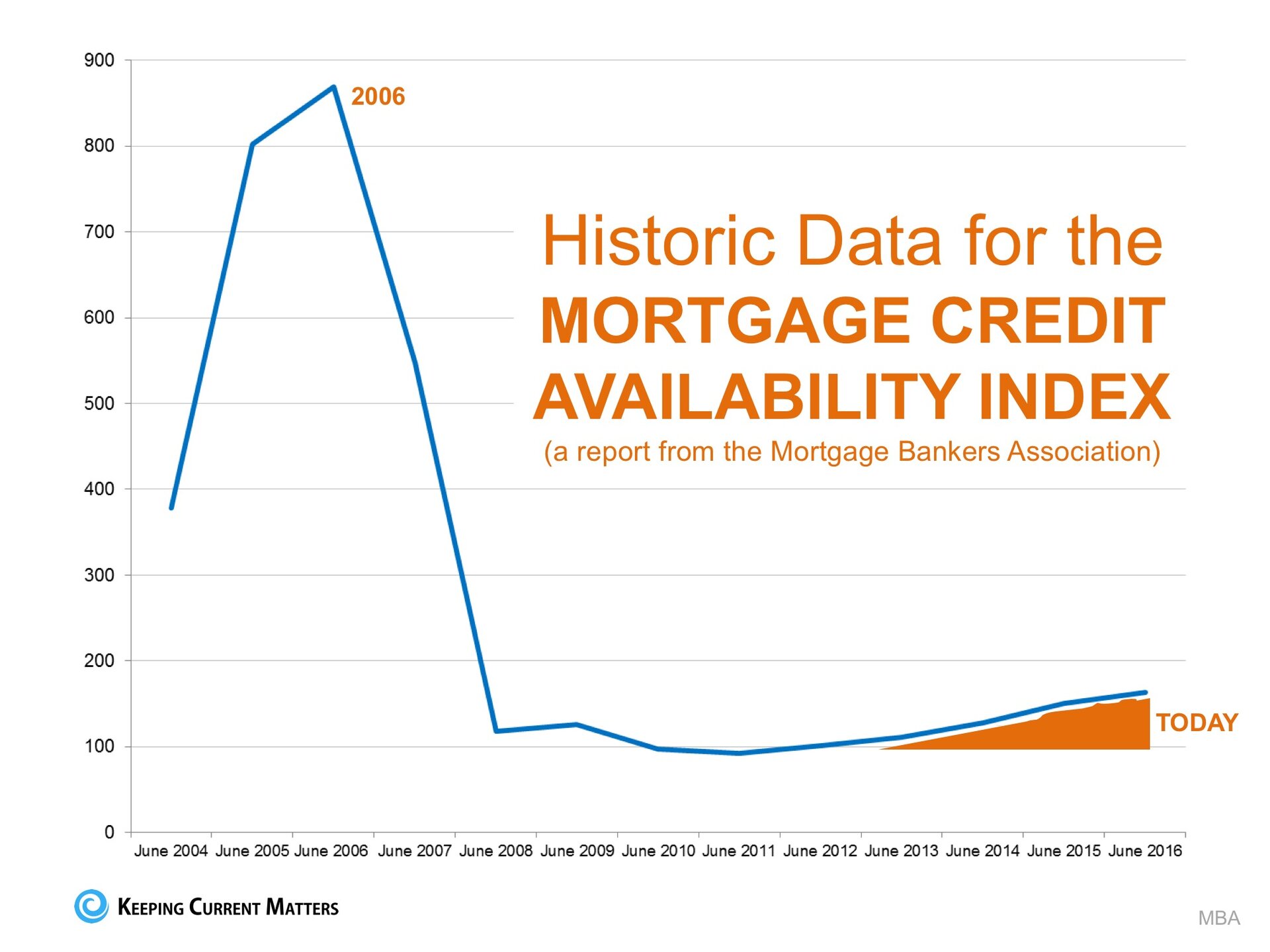

However, if we look further back at the index we see quite a different story.Mortgage Credit Availability Today Compared to 2006

The graph below shows the index going back to 2004, and the first graph we showed you above is represented by the small, orange, triangular section all the way in the lower-right corner. As this visual easily illustrates, today's index is nowhere near the levels it shot up to in 2006.

As this visual easily illustrates, today's index is nowhere near the levels it shot up to in 2006.Bottom Line

Mortgage credit is definitely easing. However, we are not coming close to the lax standards that caused the housing crisis of last decade.Monday, September 19, 2016

Why Getting Pre-Approved Should Be Your First Step

In many markets across the country, the amount of buyers searching for their dream homes greatly outnumbers the amount of homes for sale. This has led to a competitive marketplace where buyers often need to stand out. One way to show you are serious about buying your dream home is to get pre-qualified or pre-approved for a mortgage before starting your search. Even if you are in a market that is not as competitive, knowing your budget will give you the confidence of knowing if your dream home is within your reach. Freddie Mac lays out the advantages of pre-approval in the My Home section of their website: In many markets across the country, the amount of buyers searching for their dream homes greatly outnumbers the amount of homes for sale. This has led to a competitive marketplace where buyers often need to stand out. One way to show you are serious about buying your dream home is to get pre-qualified or pre-approved for a mortgage before starting your search. Even if you are in a market that is not as competitive, knowing your budget will give you the confidence of knowing if your dream home is within your reach. Freddie Mac lays out the advantages of pre-approval in the My Home section of their website:"It's highly recommended that you work with your lender to get pre-approved before you begin house hunting. Pre-approval will tell you how much home you can afford and can help you move faster, and with greater confidence, in competitive markets."One of the many advantages of working with a local real estate professional is that many have relationships with lenders who will be able to help you with this process. Once you have selected a lender, you will need to fill out their loan application and provide them with important information regarding "your credit, debt, work history, down payment and residential history." Freddie Mac describes the 4 Cs that help determine the amount you will be qualified to borrow:

Bottom LineMany potential home buyers overestimate the down payment and credit scores needed to qualify for a mortgage today. If you are ready and willing to buy, you may be pleasantly surprised at your ability to do so as well. |

Saturday, September 17, 2016

Friday, September 16, 2016

4 Colors That Turn Off Buyers

Could the wrong shade of paint dampen interest in a home? As a real estate pro, you can point sellers in the right direction when they're considering color updates.

Read more: 3 Surprising Paint Colors Home Owners Hate

First, take note of palettes consumers tell researchers they like: The favorite color combos for exteriors are white and gray, beige and taupe, and slate and black, according to the 2013 National Home Color Survey. On the inside, neutral wins too. The most popular 2016 colors include grays and shades of white, as well as natural-looking greens.

Although it's tough to prove, a Zillow Digs analysis of 50,000 photos of recently sold homes even suggests homes with creamy yellow or wheat-colored kitchens, light green or khaki bedrooms, dove or light gray living rooms, and mauve or lavender dining rooms sold for $1,100 to $1,300 more than properties decorated with less popular colors.

So, what are the paint chips your clients should avoid? Credit.com highlights the following findings based on studies of colors:

- Slate gray: While gray is an on-trend color at the moment, consumers aren’t fans of all shades of gray. Dove and light grays tend to be favorites, but consumers are more leery of dark grays. Indeed, one study even went so far as to suggest that painting a dining room a slate color could cause a home owner to lose $1,112 on their home sale. Instead, buyers say they prefer shades of mauve, eggplant, and lavender in the dining room.

- Terracotta: This shade of orange doesn’t tend to be a hit with home buyers. In fact, be cautious around orange in general. Surveys have found orange to be one of the least-liked colors in the world (blue is the favorite color globally.).

- Dark brown: The color is so disliked that the Australian government even considered using it on cigarette packaging to try to get people to stop smoking. In the end, they opted for brownish-olive green, but the fact the color was in the running should say enough.

- Off-white or eggshell: Painting walls white can sometimes be a good choice. However, if the space is small or dark, such as in a kitchen, white walls can make a room look “dead” and “flat,” designer Emily Henderson told Credit.com.

Thursday, September 15, 2016

Interest Rates Remain at Historic Lows... But for How Long?

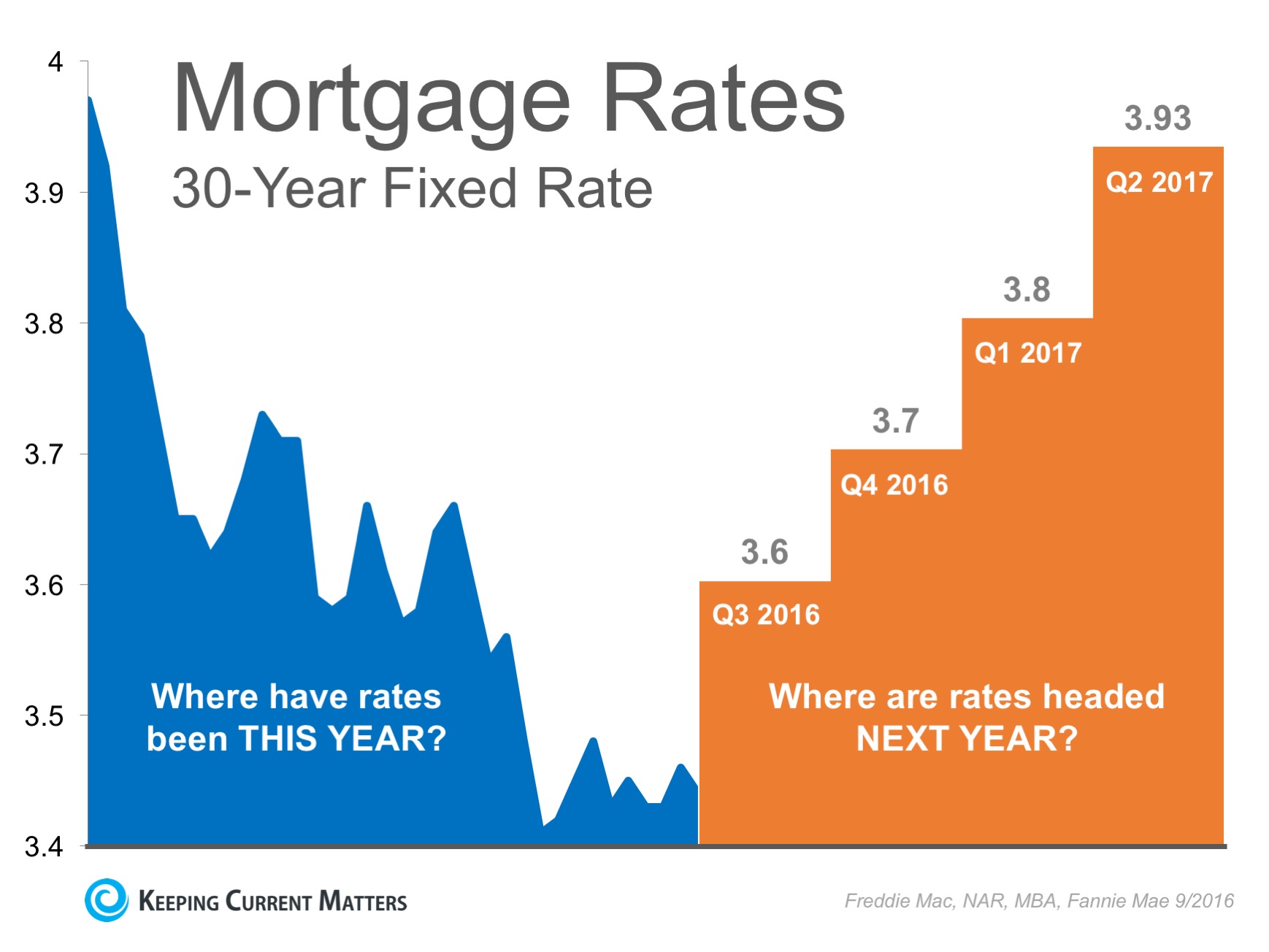

The interest rate you pay on your home mortgage has a direct impact on your monthly payment; The higher the rate, the greater your payment will be. That is why it is important to look at where the experts believe rates are headed when deciding to buy now or wait until next year. The 30-year fixed mortgage rate has fallen half a percentage point since the beginning of the year and has remained at or below 3.5% for the last 11 weeks according to Freddie Mac's Primary Mortgage Market Survey. The chart below shows how far rates have fallen this year (on the left), and uses an average of the projections from Freddie Mac, Fannie Mae, the Mortgage Bankers Association and National Association of Realtors (on the right). As you can see, interest rates are projected to increase steadily over the course of the next 12 months.

The interest rate you pay on your home mortgage has a direct impact on your monthly payment; The higher the rate, the greater your payment will be. That is why it is important to look at where the experts believe rates are headed when deciding to buy now or wait until next year. The 30-year fixed mortgage rate has fallen half a percentage point since the beginning of the year and has remained at or below 3.5% for the last 11 weeks according to Freddie Mac's Primary Mortgage Market Survey. The chart below shows how far rates have fallen this year (on the left), and uses an average of the projections from Freddie Mac, Fannie Mae, the Mortgage Bankers Association and National Association of Realtors (on the right). As you can see, interest rates are projected to increase steadily over the course of the next 12 months.

How Will This Impact Your Mortgage Payment?

Depending on the amount of the loan that you secure, a half of a percent (.5%) increase in interest rate can increase your monthly mortgage payment significantly. According to CoreLogic's latest Home Price Index, national home prices have appreciated 6.0% over the last year and are predicted to be 5.4% higher next year. If both the predictions of home prices and interest rate increases become a reality, families will wind up paying considerably more for their next home.Bottom Line

Even a small increase in interest rate can impact your family's wealth. Meet with a local real estate professional to evaluate your ability to purchase your dream home.Tuesday, September 13, 2016

5 Reasons to Sell This Fall

School is back in session, the holidays are right around the corner, you might not think that now is the best time to sell your house. But with inventory below historic numbers and demand still strong, you could be missing out on a great opportunity for your family. School is back in session, the holidays are right around the corner, you might not think that now is the best time to sell your house. But with inventory below historic numbers and demand still strong, you could be missing out on a great opportunity for your family.Here are five reasons why you should consider selling your house this fall:1. Demand Is StrongThe latest Realtors' Confidence Index from the National Association of Realtors (NAR) shows that buyer demand remains very strong throughout the vast majority of the country. These buyers are ready, willing and able to purchase... and are in the market right now! Take advantage of the buyer activity currently in the market.2. There Is Less Competition NowAccording to NAR's latest Existing Home Sales Report, the supply of homes for sale is still under the 6-month supply that is needed for a normal housing market at 4.7-months. This means, in most areas, there are not enough homes for sale to satisfy the number of buyers in that market. This is good news for home prices. However, additional inventory is about to come to market. There is a pent-up desire for many homeowners to move, as they were unable to sell over the last few years because of a negative equity situation. Homeowners are now seeing a return to positive equity as real estate values have increased over the last two years. Many of these homes will be coming to the market this fall. Also, as builders regain confidence in the market, new construction of single-family homes is projected to continue to increase over the next two years, reaching historic levels by 2017. Last month's new home sales numbers show that many buyers who have not been able to find their dream home within the existing inventory have turned to new construction to fulfill their needs. The choices buyers have will continue to increase. Don't wait until all this other inventory of homes comes to market before you sell.3. The Process Will Be QuickerFannie Mae announced that they anticipate an acceleration in home sales that will surpass 2007's pace. As the market heats up, banks will be inundated with loan inquiries causing closing-time lines to lengthen. Selling now will make the process quicker & simpler.4. There Will Never Be a Better Time to Move UpIf you are moving up to a larger, more expensive home, consider doing it now. Prices are projected to appreciate by 5.3% over the next year, according to CoreLogic. If you are moving to a higher-priced home, it will wind up costing you more in raw dollars (both in down payment and mortgage payment) if you wait. According to Freddie Mac's latest report, you can also lock-in your 30-year housing expense with an interest rate around 3.46% right now. Interest rates are projected to increase moderately over the next 12 months. Even a small increase in rate will have a big impact on your housing cost.5. It's Time to Move On with Your LifeLook at the reason you decided to sell in the first place and determine whether it is worth waiting. Is money more important than being with family? Is money more important than your health? Is money more important than having the freedom to go on with your life the way you think you should? Only you know the answers to the questions above. You have the power to take control of the situation by putting your home on the market. Perhaps the time has come for you and your family to move on and start living the life you desire.That is what is truly important. |

Friday, September 9, 2016

HOME PRICES UP 5.6% ACROSS THE COUNTRY!

![Home Prices Up 5.61% Across The Country! [INFOGRAPHIC] | Keeping Current Matters](http://www.keepingcurrentmatters.com/wp-content/uploads/2016/09/20160909-KCM-ENG.jpg)

Some Highlights:

- The Federal Housing Finance Agency (FHFA) recently released their latest Quarterly Home Price Index report.

- In the report, home prices are compared both regionally and by state.

- Based on the latest numbers, if you plan on relocating to another state, waiting to move may end up costing you more!

- Vermont was the only one state where home prices are actually lower than they were last year.

Tuesday, September 6, 2016

Why Is There So Much Paperwork to Sign to Get a Mortgage?

We are often asked why there is so much paperwork mandated by the bank for a mortgage loan application when buying a home today. It seems that the bank needs to know everything about us and requires three separate sources to validate each and every entry on the application form. Many buyers are being told by friends and family that the process was a hundred times easier when they bought their home ten to twenty years ago. There are two very good reasons that the loan process is much more onerous on today's buyer than perhaps any time in history.

We are often asked why there is so much paperwork mandated by the bank for a mortgage loan application when buying a home today. It seems that the bank needs to know everything about us and requires three separate sources to validate each and every entry on the application form. Many buyers are being told by friends and family that the process was a hundred times easier when they bought their home ten to twenty years ago. There are two very good reasons that the loan process is much more onerous on today's buyer than perhaps any time in history.1. The government has set new guidelines that now demand that the bank prove beyond any doubt that you are indeed capable of affording the mortgage.

During the run-up in the housing market, many people 'qualified' for mortgages that they could never pay back. This led to millions of families losing their home. The government wants to make sure this can't happen again.2. The banks don't want to be in the real estate business.

Over the last seven years, banks were forced to take on the responsibility of liquidating millions of foreclosures and also negotiating another million plus short sales. Just like the government, they don't want more foreclosures. For that reason, they need to double (maybe even triple) check everything on the application.However, there is some good news in the situation.

The housing crash that mandated that banks be extremely strict on paperwork requirements also allows you to get a mortgage interest rate as low as 3.43%, the latest reported rate from Freddie Mac. The friends and family who bought homes ten or twenty ago experienced a simpler mortgage application process but also paid a higher interest rate (the average 30 year fixed rate mortgage was 8.12% in the 1990's and 6.29% in the 2000's). If you went to the bank and offered to pay 7% instead of less than 4%, they would probably bend over backwards to make the process much easier.Bottom Line

Instead of concentrating on the additional paperwork required, let's be thankful that we are able to buy a home at historically low rates.Saturday, September 3, 2016

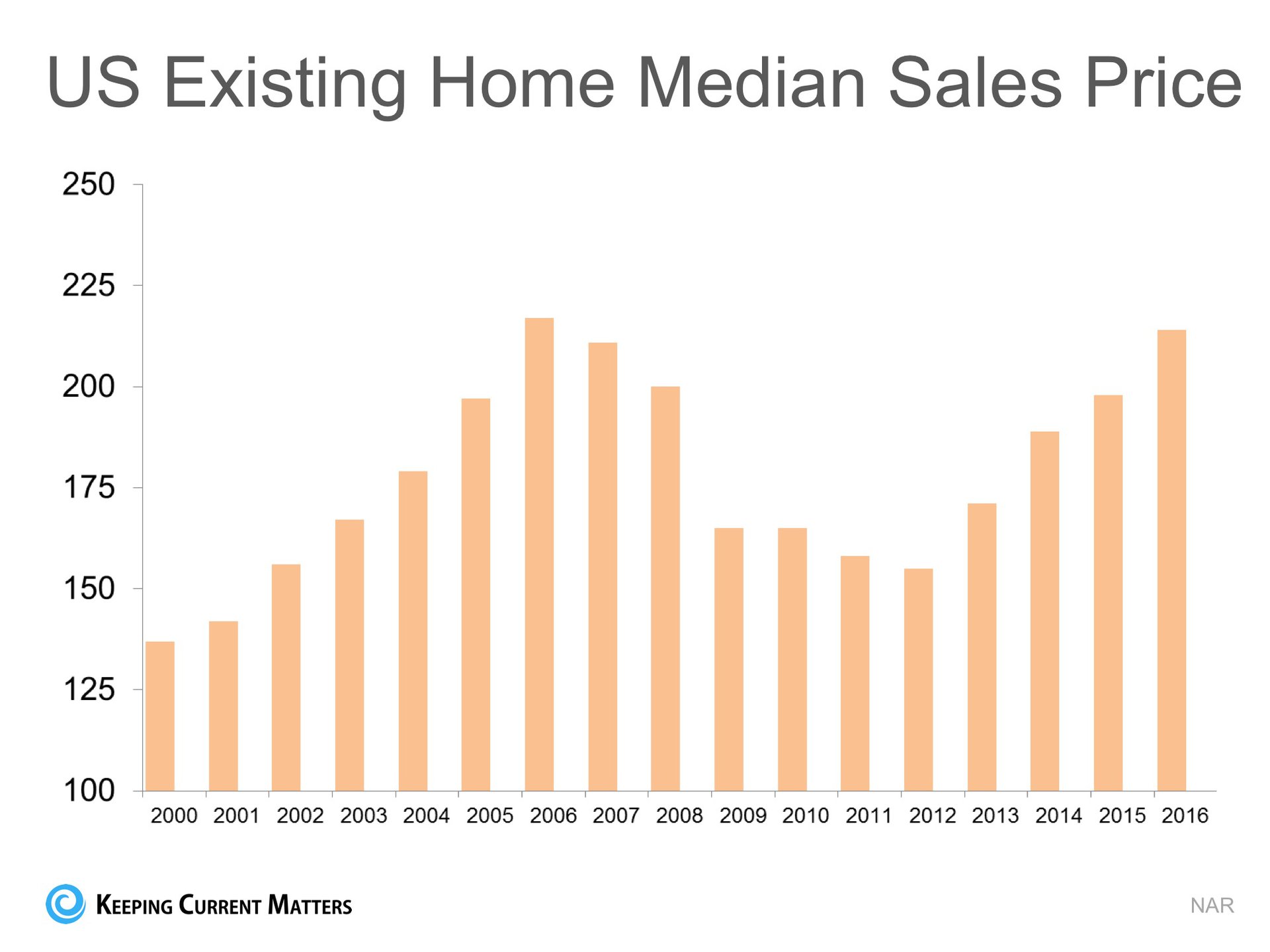

Home Values: DEFINITELY NOT in Bubble Range!!

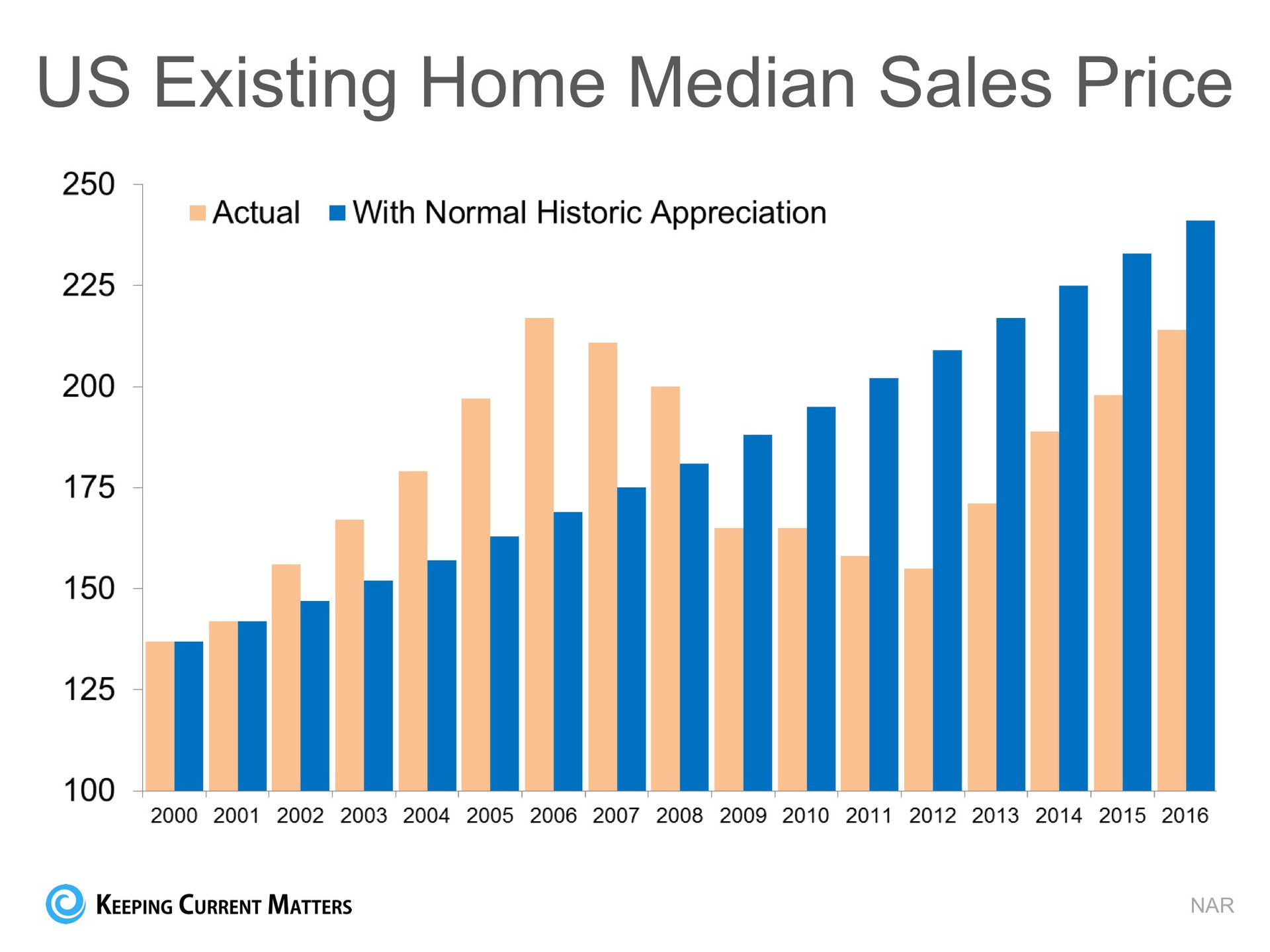

There are some industry pundits claiming that residential home values have risen too quickly and that current levels are on the verge of another housing bubble. It is easy to see how this thinking has taken form if we look at a graph of home prices from 2000 to today. There are some industry pundits claiming that residential home values have risen too quickly and that current levels are on the verge of another housing bubble. It is easy to see how this thinking has taken form if we look at a graph of home prices from 2000 to today.  The graph definitely looks like a rollercoaster ride. And, as prices begin to reach 2006 levels again, it "seems logical" that the next part of the ride would be downhill. However, this graph includes the anomaly of the price bubble and the correction (the housing crash). The graph definitely looks like a rollercoaster ride. And, as prices begin to reach 2006 levels again, it "seems logical" that the next part of the ride would be downhill. However, this graph includes the anomaly of the price bubble and the correction (the housing crash).What if the bubble & bust didn't occur?Let's assume that instead of the rise and fall in home prices that we saw last decade, we just had normal historic appreciation from 2000 to today. According to the 100+ experts that are surveyed for the Home Price Expectation Survey, normal annual appreciation for residential single family homes from 1987 to 1999 was 3.6%. Starting with the median home price in 2000, we added 3.6% to it each year since then. Here is that graph intermixed with the above graph. What this shows us is that, had the bubble and crash not occurred and instead we just had normal annual appreciation over this period, prices would actually be greater than they are today. What this shows us is that, had the bubble and crash not occurred and instead we just had normal annual appreciation over this period, prices would actually be greater than they are today.Bottom LineThere is no reason for alarm as prices seem to be right in line with where they should be |

Subscribe to:

Posts (Atom)