Tuesday, December 31, 2019

Saturday, December 28, 2019

December 2019: The Buyer Stakes Are High Because Inventory Is Low

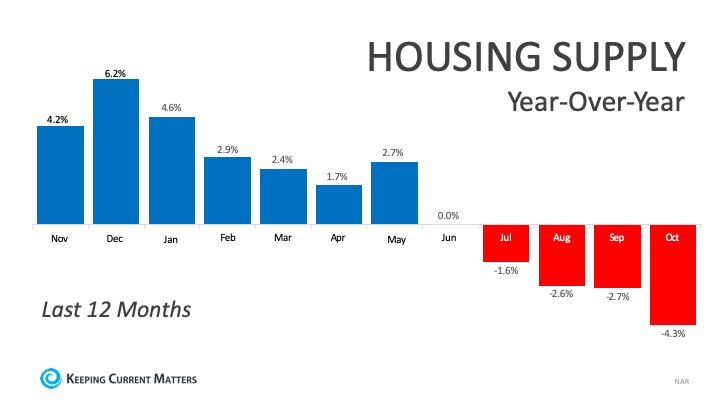

Even though the month’s supply of inventory is not increasing, ironically, the number of homes for sale is. This means homes are coming up for sale, but they’re being sold quickly. The graph below shows the year-over-year change in inventory over the last 12 months.

Even though the month’s supply of inventory is not increasing, ironically, the number of homes for sale is. This means homes are coming up for sale, but they’re being sold quickly. The graph below shows the year-over-year change in inventory over the last 12 months. As depicted above, the percentage of available inventory has fallen for four consecutive months when compared to the previous year.

As depicted above, the percentage of available inventory has fallen for four consecutive months when compared to the previous year.

So, what does this mean? If you’re a buyer, be sure to get pre-approved for a mortgage and be ready to make a competitive offer, so you can move quickly. Chances are, homes high on your wish list are likely going to go fast.

Bottom Line

If you’re thinking of buying a home, make sure you’re taking the right steps at the beginning of the process, so you’re a top contender if you ultimately find yourself in a bidding war. Reach out to a local real estate professional to determine what you need to do to make your move toward homeownership.

Friday, December 27, 2019

Thursday, December 26, 2019

Wednesday, December 25, 2019

Tuesday, December 24, 2019

Sunday, December 22, 2019

Friday, December 20, 2019

Millennials Are on the Move as First-Time Homebuyers [INFOGRAPHIC]

![Is Your First Home Now Within Your Grasp? [INFOGRAPHIC] | Keeping Current Matters](https://files.keepingcurrentmatters.com/wp-content/uploads/2019/12/05114658/20191206-NM-scaled.jpg)

Some Highlights:

- According to NAR’s latest Profile of Home Buyers & Sellers, the median age of all first-time homebuyers is 32.

- With more millennials entering a homebuying phase of life, they are driving a large portion of the buyer appetite in the market, keeping buyer activity strong.

- More and more “old millennials” (ages 25-36) are realizing that homeownership is now within their grasp, and they’re actively dominating the first-time homebuyer market!

Thursday, December 19, 2019

Have You Budgeted for Closing Costs?

Saving for a down payment is a key step in the homebuying process, and it’s not the only piece you need to include in your budget. Another factor that’s important to plan for is the closing costs required to obtain a mortgage.

Saving for a down payment is a key step in the homebuying process, and it’s not the only piece you need to include in your budget. Another factor that’s important to plan for is the closing costs required to obtain a mortgage.What Are Closing Costs?

According to Trulia,

“When you close on a home, a number of fees are due. They typically range from 2% to 5% of the total cost of the home, and can include title insurance, origination fees, underwriting fees, document preparation fees, and more.”

For those who buy a $250,000 home, for example, that amount could be between $5,000 and $12,500 in closing fees. Keep in mind, if you’re in the market for a home above this price range, your costs could be significantly greater. As mentioned before,

Closing costs are typically between 2% and 5% of your purchase price.

Trulia gives more great advice, saying,

“There will be lots of paperwork in front of you on closing day, and not enough time to read them all. Work closely with your real estate agent, lender, and attorney, if you have one, to get all the documents you need ahead of time.The most important thing to read is the closing disclosure, which shows your loan terms, final closing costs, and any outstanding fees. You’ll get this form about three days before closing since, once you (the borrower) sign it, there’s a three-day waiting period before you can sign the mortgage loan docs. If you have any questions about the numbers or what any of the mortgage terms mean, this is the time to ask—your real estate agent is a great resource for getting you all the answers you need.”

Bottom Line

Reach out to your lender and a local real estate professional to discuss the homebuying process, to be sure your plan includes budgeting for what you need to purchase your dream home – without any surprises!

Wednesday, December 18, 2019

Have You Outgrown Your Home?

It may seem hard to imagine that the home you’re in today – whether it’s your starter home or just one you’ve fallen in love with along the way – might not be your forever home.

It may seem hard to imagine that the home you’re in today – whether it’s your starter home or just one you’ve fallen in love with along the way – might not be your forever home.

The good news is, it’s okay to admit if your house no longer fits your needs.

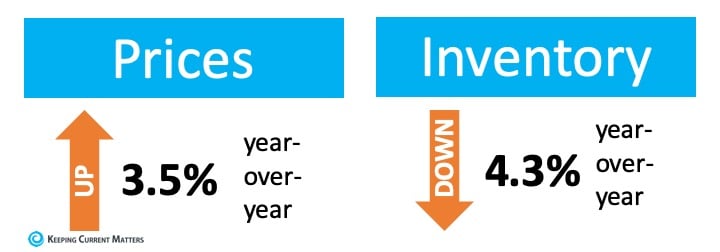

According to the latest Home Price Insights from CoreLogic, prices have appreciated 3.5% year-over-year. At the same time, the National Association of Realtors (NAR) reports inventory has dropped 4.3% from one year ago. These two statistics are directly related to one another. As inventory has decreased and demand has increased, prices have been driven up.

These two statistics are directly related to one another. As inventory has decreased and demand has increased, prices have been driven up.

These two statistics are directly related to one another. As inventory has decreased and demand has increased, prices have been driven up.

This is great news if you own a home and are thinking about selling. The equity in your house has likely risen as prices have increased. Even better is the fact that there’s a large pool of buyers out there searching for the American dream, and your home may be high on their wish list.

Bottom Line

If you think you’ve outgrown your home, reach out to a real estate professional to discuss local market conditions and determine if now is the best time for you to sell.

Tuesday, December 17, 2019

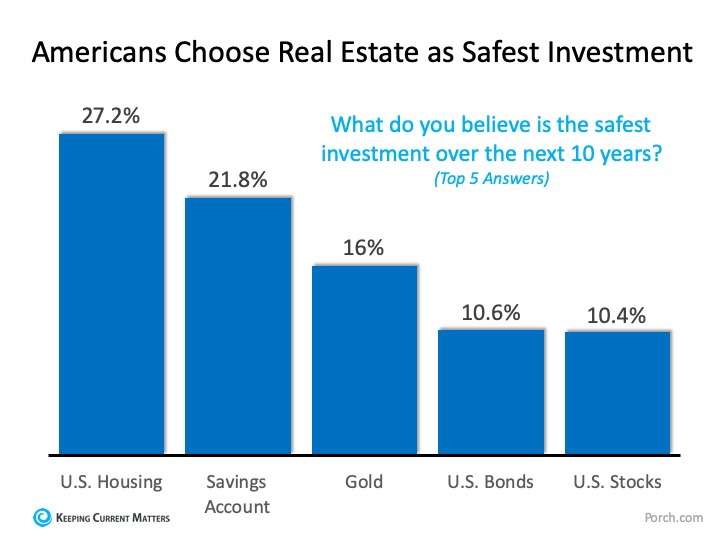

What is the Best Investment for Americans?

Some are reporting that there is trepidation regarding the real estate market in the United States. Apparently, the American people are quite comfortable.

Some are reporting that there is trepidation regarding the real estate market in the United States. Apparently, the American people are quite comfortable.

Porch.com, a major network helping homeowners with their renovation projects, recently conducted a survey which asked Americans:

“What do you believe is the safest investment over the next 10 years?”

U.S. housing came in at number one, beating out other investments such as gold, stocks, bonds, and savings.

Here is a graph showing the top five investments Americans selected: The findings of the Porch.com survey also coincide with two previous surveys done earlier this year:

The findings of the Porch.com survey also coincide with two previous surveys done earlier this year:

The findings of the Porch.com survey also coincide with two previous surveys done earlier this year:- The Federal Reserve Bank’s 2019 Consumer Expectations Housing Survey reported that 65% of Americans believe homeownership is a good financial investment, and that the percentage has increased in each of the last four years.

- The Gallup survey showed that Americans have picked real estate as the “best” investment for six straight years.

Bottom Line

Based on all three surveys done this year, we can see that Americans still believe in homeownership as a great investment, and that feeling continues to grow.

Monday, December 16, 2019

Saturday, December 14, 2019

Friday, December 13, 2019

2 Myths Holding Back Home Buyers

In a recent article, First American shared how millennials are not really any different from previous generations when it comes to the goal of homeownership; it is still a huge part of their American Dream. The piece, however, also reveals,

In a recent article, First American shared how millennials are not really any different from previous generations when it comes to the goal of homeownership; it is still a huge part of their American Dream. The piece, however, also reveals,“Saving for a down payment is one of the biggest obstacles faced by first-time home buyers. Dispelling the 20 percent down payment myth could open the path to homeownership for many more.”

Myth #1: “I Need a 20% Down Payment”

Buyers often overestimate how much they need to qualify for a home loan. According to the same article:

“Americans still overestimate the qualifications needed to get a mortgage, resulting in qualified potential buyers not even considering homeownership. Indeed, the Urban Institute report revealed that 16 percent of consumers believed that the minimum down payment required by lenders is 20 percent or more, and another 40 percent didn’t know at all.”

While many potential buyers still think they need to put at least 20% down for the home of their dreams, they often don’t realize how many assistance programs are available with as little as 3% down. With a little research, many renters may actually be able to enter the housing market sooner than they ever imagined.

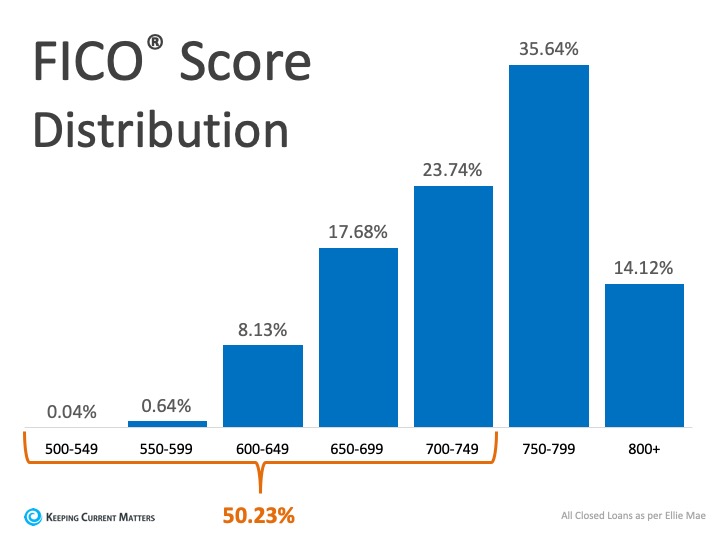

Myth #2: “I Need a 780 FICO® Score or Higher”

In addition to down payments, buyers are also often confused about the FICO® score it takes to qualify for a mortgage, believing a ‘good’ credit score is 780 or higher.

To debunk this myth, let’s take a look at Ellie Mae’s latest Origination Insight Report, which focuses on recently closed (approved) loans. As indicated in the chart above, 50.23% of approved mortgages had a credit score of 500-749.

As indicated in the chart above, 50.23% of approved mortgages had a credit score of 500-749.

As indicated in the chart above, 50.23% of approved mortgages had a credit score of 500-749.Bottom Line

Whether buying your first home or moving up to your dream home, knowing your options will make the mortgage process easier. Believe it or not – your dream home may already be within your reach.

Thursday, December 12, 2019

Forget the Price of the Home. The Cost is What Matters.

Home buying activity (demand) is up, and the number of available listings (supply) is down. When demand outpaces supply, prices appreciate. That’s why firms are beginning to increase their projections for home price appreciation going forward. As an example, CoreLogic increased their 12-month projection for home values from 4.5% to 5.6% over the last few months.

Home buying activity (demand) is up, and the number of available listings (supply) is down. When demand outpaces supply, prices appreciate. That’s why firms are beginning to increase their projections for home price appreciation going forward. As an example, CoreLogic increased their 12-month projection for home values from 4.5% to 5.6% over the last few months.

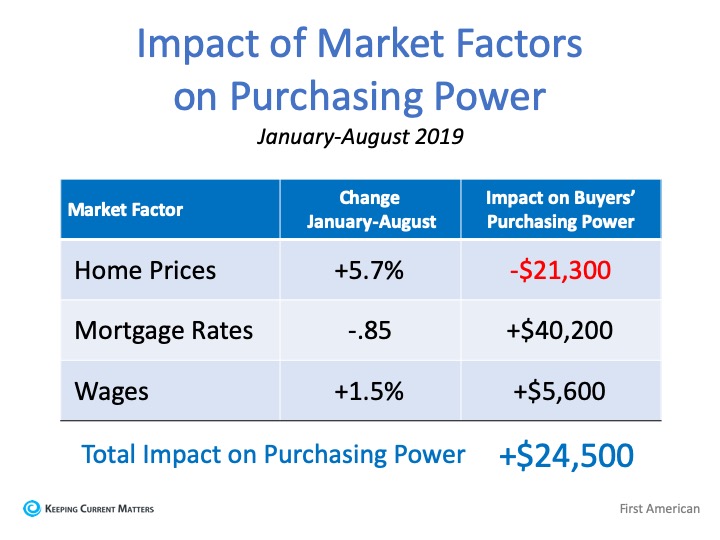

The reacceleration of home values will cause some to again voice concerns about affordability. Just last week, however, First American came out with a data analysis that explains how price is not the only market factor that impacts affordability. They studied prices, mortgage rates, and wages from January through August of this year. Here are their findings:

Home Prices

“In January 2019, a family with the median household income in the U.S. could afford to buy a $373,900 house. By August, that home had appreciated to $395,000, an increase of $21,100.”

Mortgage Interest Rates

“The 0.85 percentage point drop in mortgage rates from January 2019 through August 2019 increased affordability by 9.7%. That translates to a $40,200 improvement in house-buying power in just eight months.”

Wage Growth

“As rates have fallen in 2019, the economy has continued to perform well also, resulting in a tight labor market and wage growth. Wage growth pushes household incomes upward, which were 1.5% higher in August compared with January. The growth in household income increased consumer house-buying power by 1.5%, pushing house-buying power up an additional $5,600.”

When all three market factors are combined, purchasing power increased by $24,500, thus making home buying more affordable, not less affordable. Here is a table that simply shows the data:

Bottom Line

In the article, Mark Fleming, Chief Economist at First American, explained it best:

“Focusing on nominal house price changes alone as an indication of changing affordability, or even the relationship between nominal house price growth and income growth, overlooks what matters more to potential buyers – surging house-buying power driven by the dynamic duo of mortgage rates and income growth. And, we all know from experience, you buy what you can afford to pay per month.”

Wednesday, December 11, 2019

Tuesday, December 10, 2019

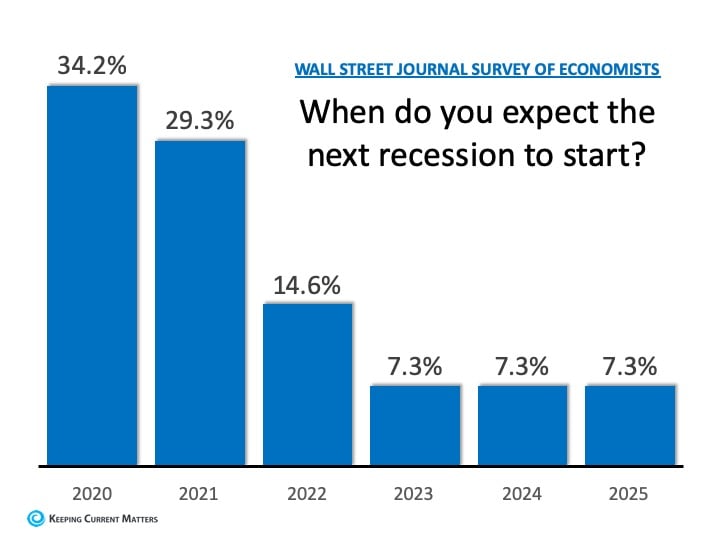

How Long Can This Economic Recovery Last?

The economy is currently experiencing the longest recovery in our nation’s history. The stock market has hit record highs, while unemployment rates are at record lows. Home price appreciation is beginning to reaccelerate. This begs the question: How long can this economic recovery last?

The economy is currently experiencing the longest recovery in our nation’s history. The stock market has hit record highs, while unemployment rates are at record lows. Home price appreciation is beginning to reaccelerate. This begs the question: How long can this economic recovery last?

The Wall Street Journal (WSJ) Survey of Economists recently called for an economic slowdown (recession) in the near future. The most recent survey, however, now shows the economists are pushing that timetable back. When asked when they expect a recession to start, 42.5% of the economists in the previous survey projected between now and the end of 2020. The most recent survey showed that percentage drop to 34.2%. Here are the most current results: Like the economists surveyed by the WSJ, most experts are still predicting a recession will likely occur sometime in the next few years. However, many are pushing back the date for the economic slowdown.

Like the economists surveyed by the WSJ, most experts are still predicting a recession will likely occur sometime in the next few years. However, many are pushing back the date for the economic slowdown.

Like the economists surveyed by the WSJ, most experts are still predicting a recession will likely occur sometime in the next few years. However, many are pushing back the date for the economic slowdown.Bottom Line

Real estate is impacted by the economy (and the consumer’s belief in the strength of the economy). The fact that most economic experts are calling for the recovery to continue through 2020 means the housing market will also remain strong for the foreseeable future.

Monday, December 9, 2019

Sunday, December 8, 2019

Friday, December 6, 2019

The True Cost of Not Owning Your Home

There are great advantages to owning a home, yet many people continue to rent. The financial benefits are just some of the reasons why homeownership has been a part of the long-standing American dream.

There are great advantages to owning a home, yet many people continue to rent. The financial benefits are just some of the reasons why homeownership has been a part of the long-standing American dream.

Realtor.com reported that:

“Buying remains the more attractive option in the long term – that remains the American dream, and it’s true in many markets where renting has become really the shortsighted option…as people get more savings in their pockets, buying becomes the better option.”

Why is owning a home financially better than renting?

Here are the top 5 financial benefits of homeownership:

- Homeownership is a form of forced savings.

- Homeownership provides tax savings.

- Homeownership allows you to lock in your monthly housing cost.

- Buying a home is less expensive than renting.

- No other investment lets you live inside of it.

Studies have also shown that a homeowner’s net worth is 44x greater than that of a renter.

A family that purchased a median-priced home at the start of 2019 would build more than

$37,750 in family wealth over the next five years with projected price appreciation alone.

$37,750 in family wealth over the next five years with projected price appreciation alone.

Some argue that renting eliminates the cost of taxes and home repairs, but every potential renter must realize that all the expenses the landlord incurs are already baked into the rent payment – along with a profit margin!

Bottom Line

Owning a home has many social and financial benefits that cannot be achieved by renting. Reach out to a Real Estate Professional to determine if buying a home is your best move.

Subscribe to:

Comments (Atom)