Friday, November 29, 2019

Thursday, November 28, 2019

Wednesday, November 27, 2019

Monday, November 25, 2019

Saturday, November 23, 2019

Thursday, November 21, 2019

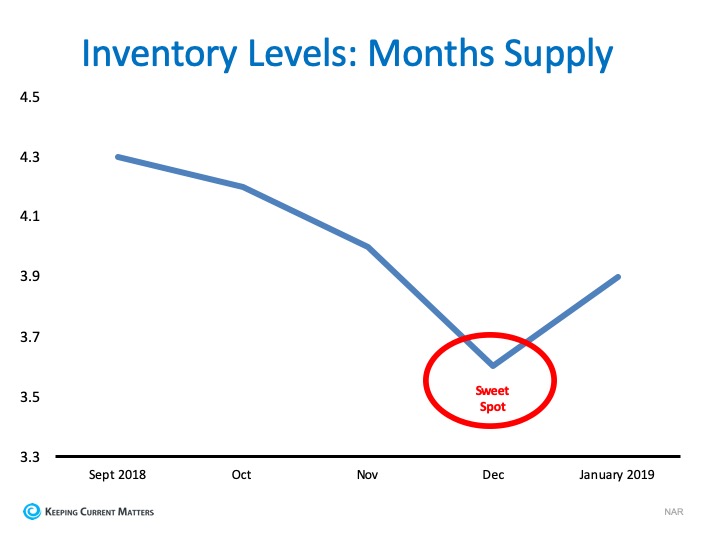

Many sellers believe spring is the best time to put their homes on the market because buyer demand traditionally increases at that time of year. What they don’t realize is if every homeowner believes the same thing, then that’s when they’ll have the most competition.

Many sellers believe spring is the best time to put their homes on the market because buyer demand traditionally increases at that time of year. What they don’t realize is if every homeowner believes the same thing, then that’s when they’ll have the most competition.So, what’s the #1 reason to list your house in the winter? Less competition.

Housing supply traditionally shrinks at this time of year, so the choices buyers have will be limited. The chart below was created using the months supply of listings from the National Association of Realtors. As you can see, the ‘sweet spot’ to list your house for the most exposure naturally occurs in the late fall and winter months (November – January).

As you can see, the ‘sweet spot’ to list your house for the most exposure naturally occurs in the late fall and winter months (November – January).

As you can see, the ‘sweet spot’ to list your house for the most exposure naturally occurs in the late fall and winter months (November – January).

Temperatures aren’t the only thing that heats up in the spring – so do listings! In 2018, listings increased from December to May. Don’t wait for these listings and the competition that comes with them to come to the market before you decide to list your house.

In 2018, listings increased from December to May. Don’t wait for these listings and the competition that comes with them to come to the market before you decide to list your house.

In 2018, listings increased from December to May. Don’t wait for these listings and the competition that comes with them to come to the market before you decide to list your house.Added Bonus: Serious Buyers Are Out in the Winter

At this time of year, purchasers who are serious about buying a home will be in the marketplace. You and your family will not be bothered and inconvenienced by mere ‘lookers.’ The lookers are at the mall or online doing their holiday shopping.

Bottom Line

If you’ve been debating whether or not to sell your house and are curious about market conditions in your area, talk with a local real estate professional who can help you decide the best time to list your house.

Tuesday, November 19, 2019

To understand today’s complex real estate market, it is critical to have a local, trusted advisor on your side – for more reasons than you may think.

To understand today’s complex real estate market, it is critical to have a local, trusted advisor on your side – for more reasons than you may think.

In real estate today, there are essentially three different price points in the market: the starter-home market, the middle-home market, and the premium or luxury market. Each one is unique, and depending on the city, the price point in these categories will vary. For example, a starter or lower-end home in San Francisco, California is much more expensive than almost any other part of the country. Let’s explore what you need to know about each of these tiers.

Starter-Home Market: This market varies by price, and these homes are typically purchased by first-time home buyers or investors looking to flip them for a profit. Across the country, homes in this space currently have less than 6 months of inventory for sale. That means there aren’t enough homes on the lower end of the market for the number of people who want to buy them. A low supply like this generally increases competition, drives bidding wars, and sets up an environment where homes sell above the listing price. According to data from the National Association of Realtors (NAR) on realtor.com,

“The desire for affordability continues to push down the inventory for homes listed for less than $200,000.00.”

Middle-Home Market: This segment is often thought of as the move-up market. Typically, the buyer in this market is moving up to a larger, more custom home with more features, all coming at a higher price. Across the country, this market is looking more balanced than the lower end of the market, meaning it has closer to a 6-month supply of inventory for sale. This market is more neutral, but leaning towards a seller’s market.

Premium & Luxury Home Market: This is the top end of the market with larger homes that have even more custom features and upgrades. Nationwide, this market is growing in the number of homes for sale. In the same realtor.com article, we can see that year-over-year inventory of homes in this tier has grown by 4.7%. Today, there are more homes available in the premium and luxury space, leading to more of a buyer’s market at this end.

Bottom Line

Depending on the segment of the market and the price point you’re looking at, you’re going to need the advice of a true local market expert to help you successfully navigate the home-buying or selling process.

Monday, November 18, 2019

If you’re searching for a home online, you’re not alone; lots of people are doing it. The question is, are you using all of your available resources, and are you using them wisely? Here’s why the Internet is a great place to start the home-buying process, and the truth on why it should never be your only go-to resource when it comes to making such an important decision.

According to the National Association of Realtors (NAR), the three most popular information sources home buyers use in the home search are:

- Online website (93%)

- Real estate agent (86%)

- Mobile/tablet website or app (73%)

Clearly, you’re not alone if you’re starting your search online; 93% of home buyers are right there with you. The even better news: 86% of buyers are also getting their information from a real estate agent at the same time.

Here are 3 top reasons why using a real estate professional in addition to a digital search is key:

1. There’s More to Real Estate Than Finding a Home Online. It’s a lonely and complicated trek around the web if you don’t have a real estate professional to also help you through the 230 possible steps you’ll face as you navigate through a real estate transaction. That’s a pretty staggering number! Determining your price, submitting an offer, and successful negotiation are just a few of these key steps in the sequence. You’ll definitely want someone who has been there before to help you through it.

2. You Need a Skilled Negotiator. In today’s market, hiring a talented negotiator could save you thousands, maybe even tens of thousands of dollars. From the original offer to the appraisal and the inspection, many of the intricate steps can get complicated and confusing. You need someone who can keep the deal together until it closes.

3. It Is Crucial to Make a Competitive and Compelling Offer. There is so much information out there in the news and on the Internet about home sales, prices, and mortgage rates. How do you know what’s specifically going on in your area? How do you know what to offer on your dream home without paying too much or offending the seller with a lowball offer?

Dave Ramsey, the financial guru, advises:

“When getting help with money, whether it’s insurance, real estate or investments, you should always look for someone with the heart of a teacher, not the heart of a salesman.”

Hiring a real estate professional who has his or her finger on the pulse of the market will make your buying experience an informed and educated one. You need someone who is going to tell you the truth, not just what they think you want to hear.

Bottom Line

If you’re ready to start your search online, don’t skip over the support of an educated and informed real estate professional. You’ll want someone at your side who can answer your questions and guide you through a process that can be complex and confusing if you go at it with the Internet alone.

Friday, November 15, 2019

Thursday, November 14, 2019

Here are four great reasons to consider buying a home today, instead of waiting.

Here are four great reasons to consider buying a home today, instead of waiting.

1. Prices Will Continue to Rise

CoreLogic’s latest Home Price Insights Report shows that home prices have appreciated by 3.6% over the last 12 months. The same report predicts prices will continue to increase at a rate of 5.8% over the next year.

The bottom in home prices has come and gone. Home values will continue to appreciate for years. Waiting no longer makes sense.

2. Mortgage Interest Rates Are Projected to Increase Next Year

The Primary Mortgage Market Survey from Freddie Mac indicates that interest rates for a 30-year mortgage have recently hovered just above 3.5%. This is great news for buyers in the market right now, because low interest rates increase your purchasing power – but don’t wait! Most experts predict rates will rise over the next 12 months. The Mortgage Bankers Association, Fannie Mae, Freddie Mac, and the National Association of Realtors are in unison, projecting that rates will increase by this time next year.

An increase in rates will impact your monthly mortgage payment. A year from now, your housing expense will increase if a mortgage is needed to buy your next home.

3. Either Way, You Are Paying a Mortgage

There are some renters who haven’t purchased a home yet because they’re uncomfortable taking on the obligation of a mortgage. Everyone should realize that, unless you’re living rent-free with your parents, you are paying a mortgage – either yours or that of your landlord.

As an owner, your mortgage payment is a form of ‘forced savings’ that allows you to have equity in your home you can tap into later in life. As a renter, you guarantee your landlord is the person with that equity.

Are you ready to put your housing costs to work for you?

4. It’s Time to Move on With Your Life

The ‘cost’ of a home is determined by two major components: the price of the home and the current mortgage rate. It appears both are on the rise.

But what if they weren’t? Would you wait?

Look at the actual reason you’re buying and decide if it is worth waiting. Whether you want to have a great place for your children to grow up, you want your family to be safer, or you just want to have control over custom renovations, maybe now is the time to buy.

Bottom Line

Buying a home sooner rather than later could lead to substantial savings. Reach out to a local real estate professional to determine if homeownership is the right choice for you and your family this fall.

Wednesday, November 13, 2019

Tuesday, November 12, 2019

The gap between the increase in personal income and residential real estate prices has been used to defend the concept that we are experiencing an affordability crisis in housing today.

The gap between the increase in personal income and residential real estate prices has been used to defend the concept that we are experiencing an affordability crisis in housing today.

It is true that home prices and wages are two key elements in any affordability equation. There is, however, an extremely important third component to that equation: mortgage interest rates.

Mortgage interest rates have fallen by more than a full percentage point from this time last year. Today’s rate is 3.75%; it was 4.86% at this time last year. This has dramatically increased a purchaser’s ability to afford a home.

Here are three reports validating that purchasing a home is in fact more affordable today than it was a year ago:

“Falling mortgage rates and slower home-price growth mean that many buyers this year are committing to lower mortgage payments than they would have faced for the same home last year. After rising at a double-digit annual pace in 2018, the principal-and-interest payment on the nation’s median-priced home – what we call the “typical mortgage payment”– fell year-over-year again.”

“At the national level, housing affordability is up from last month and up from a year ago…All four regions saw an increase in affordability from a year ago…Payment as a percentage of income was down from a year ago.”

“In 2019, the dynamic duo of lower mortgage rates and rising incomes overcame the negative impact of rising house price appreciation on affordability. Indeed, affordability reached its highest point since January 2018. Focusing on nominal house price changes alone as an indication of changing affordability, or even the relationship between nominal house price growth and income growth, overlooks what matters more to potential buyers – surging house-buying power driven by the dynamic duo of mortgage rates and income growth. And, we all know from experience, you buy what you can afford to pay per month.”

Bottom Line

Though the price of homes may still be rising, the cost of purchasing a home is actually falling. If you’re thinking of buying your first home or moving up to your dream home, make sure to reach out to a real estate professional to help you understand the difference between the two.

Monday, November 11, 2019

Sunday, November 10, 2019

Friday, November 8, 2019

Millennials have waited longer than any other generation to become homeowners, but the wait for this cohort is just about over. According to National Mortgage News,

Millennials have waited longer than any other generation to become homeowners, but the wait for this cohort is just about over. According to National Mortgage News,“Millennials, those young adults now aged 23 to 38, are now entering their peak household formation and homebuying years.”

If you’re a Millennial, you’re already well aware that you’re among a generation of those who favor fast-paced, real-time answers – and results. When you’re ready to make a decision, it’s go-time, and you probably want the latest technology at your fingertips to make it happen.

National Mortgage News agrees, stating,

“Millennials are different than previous generations—not only in their delayed homebuying but also in how they approach interactions with financial institutions, including mortgage lenders. Taking a picture of a check on their phone and depositing it without visiting a branch is not novel, it’s the way Millennials learned to do banking. They expect real-time access to account and transaction data and are frustrated when it’s not available.”

Here’s the catch – the overall speed of the homebuying process can take some time, and it might feel like it is slowing you down. When you’re ready to buy, you can make an offer and go under contract quickly, but the rest of the process might take a little longer. The same article explains why:

“When Millennials apply for a loan, the mortgage lender must qualify the borrower and determine who owns the property, how much the property is worth, and the property’s risk profile. Traditionally, this has been one of the most time-consuming and fragmented parts of the mortgage process…There are many moving pieces, each data point being sourced from a different provider, which can ultimately lead to a lengthy or delayed process.What has historically been accepted as the process norm does not align with the expectations of the most prominent generation in the home buying market today. Millennials have come to expect rapid, digital workflows in their daily purchase decisions, and in their mind, the home buying process shouldn’t be any different.”

So, where do you go from here?

If you’re pre-approved for a mortgage, that will help speed things up. But the steps it takes and the time to finalize a loan with most traditional lenders may feel like an eternity to you and your generational peers. Don’t worry, though – it’s well worth the wait when you finally get the keys to your new castle!

The financial benefits of homeownership, like increasing your net worth by building equity, and the non-financial benefits, like being able to customize and improve your space, will ultimately set you on the course to happiness, success, overall satisfaction, and much, much more.

Bottom Line

If you’re feeling like it’s go-time, reach out to a local real estate professional and get the process moving to determine if homeownership is your next best step.

Thursday, November 7, 2019

Wednesday, November 6, 2019

Tuesday, November 5, 2019

Monday, November 4, 2019

Sunday, November 3, 2019

Saturday, November 2, 2019

Subscribe to:

Comments (Atom)