Monday, September 30, 2019

Congratulations! You’ve found a home to buy and have applied for a mortgage! You’re undoubtedly excited about the opportunity to decorate your new home, but before you make any large purchases, move your money around, or make any big-time life changes, consult your loan officer – someone who will be able to tell you how your decisions will impact your home loan.

Congratulations! You’ve found a home to buy and have applied for a mortgage! You’re undoubtedly excited about the opportunity to decorate your new home, but before you make any large purchases, move your money around, or make any big-time life changes, consult your loan officer – someone who will be able to tell you how your decisions will impact your home loan.

Below is a list of Things You Shouldn’t Do After Applying for a Mortgage. Some may seem obvious, but some may not.

1. Don’t Change Jobs or the Way You Are Paid at Your Job. Your loan officer must be able to track the source and amount of your annual income. If possible, you’ll want to avoid changing from salary to commission or becoming self-employed during this time as well.

2. Don’t Deposit Cash into Your Bank Accounts. Lenders need to source your money, and cash is not really traceable. Before you deposit any amount of cash into your accounts, discuss the proper way to document your transactions with your loan officer.

3. Don’t Make Any Large Purchases Like a New Car or Furniture for Your New Home. New debt comes with it, including new monthly obligations. New obligations create new qualifications. People with new debt have higher debt to income ratios…higher ratios make for riskier loans…and sometimes qualified borrowers no longer qualify.

4. Don’t Co-Sign Other Loans for Anyone. When you co-sign, you are obligated. As we mentioned, with that obligation comes higher ratios as well. Even if you swear you will not be the one making the payments, your lender will have to count the payments against you.

5. Don’t Change Bank Accounts. Remember, lenders need to source and track assets. That task is significantly easier when there is consistency among your accounts. Before you even transfer any money, talk to your loan officer.

6. Don’t Apply for New Credit. It doesn’t matter whether it’s a new credit card or a new car. When you have your credit report run by organizations in multiple financial channels (mortgage, credit card, auto, etc.), your FICO® score will be affected. Lower credit scores can determine your interest rate and maybe even your eligibility for approval.

7. Don’t Close Any Credit Accounts. Many clients erroneously believe that having less available credit makes them less risky and more likely to be approved. Wrong. A major component of your score is your length and depth of credit history (as opposed to just your payment history) and your total usage of credit as a percentage of available credit. Closing accounts has a negative impact on both of those determinants in your score.

Bottom Line

Any blip in income, assets, or credit should be reviewed and executed in a way that ensures your home loan can still be approved. The best advice is to fully disclose and discuss your plans with your loan officer before you do anything financial in nature. They are there to guide you through the process.

Sunday, September 29, 2019

Friday, September 27, 2019

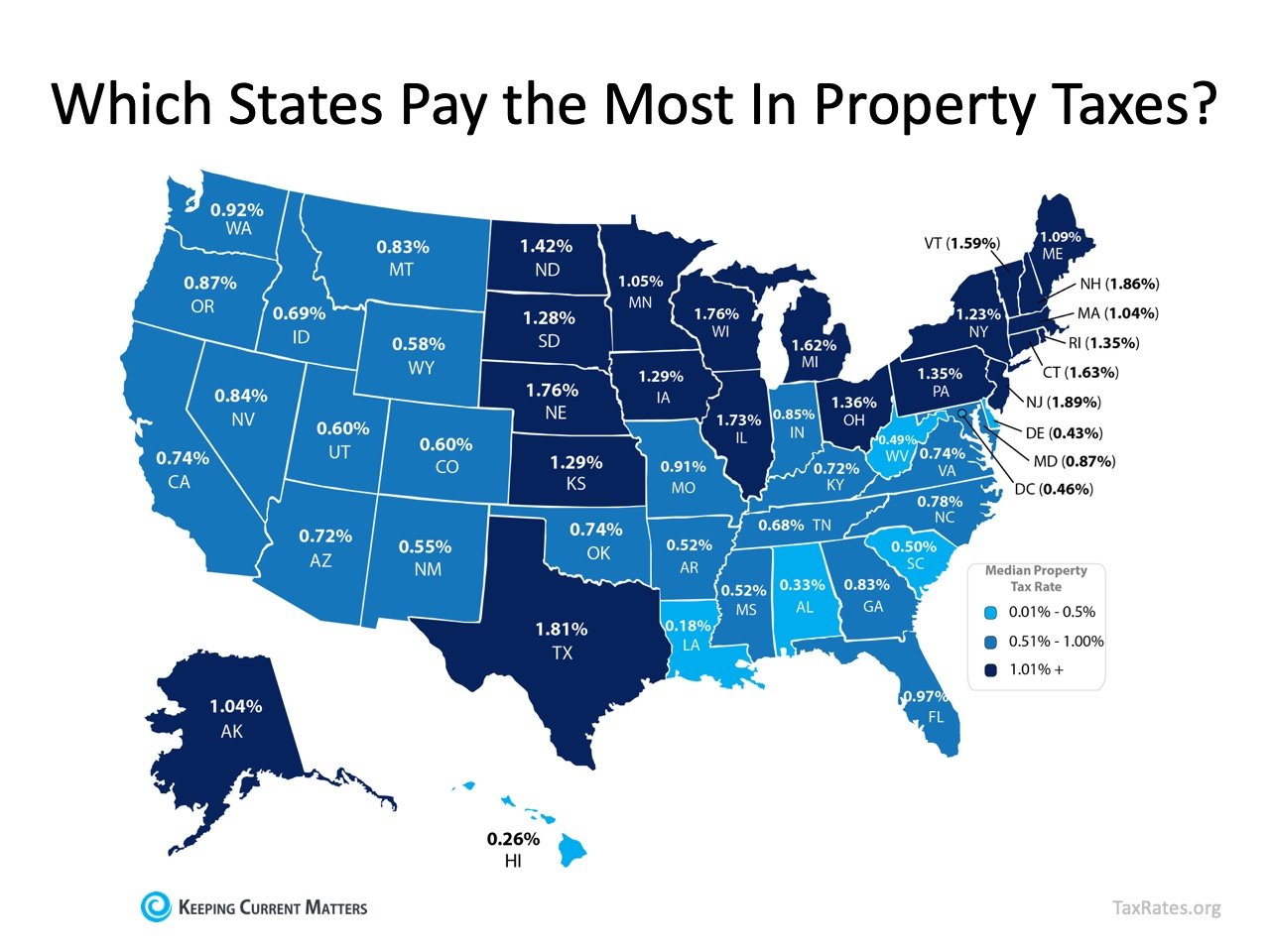

When buying a home, taxes are one of the expenses that can make a significant difference in your monthly payment. Do you know how much you might pay for property taxes in your state or local area?

When buying a home, taxes are one of the expenses that can make a significant difference in your monthly payment. Do you know how much you might pay for property taxes in your state or local area?

When applying for a mortgage, you’ll see one of two acronyms in your paperwork – P&I or PITI – depending on how you’re including your taxes in your mortgage payment.

P&I stands for Principal and Interest, and both are parts of your monthly mortgage payment that go toward paying off the loan you borrow. PITI stands for Principal, Interest, Taxes, and Insurance, and they’re all important factors to calculate when you want to determine exactly what the cost of your new home will be.

TaxRates.org defines property taxes as,

“A municipal tax levied by counties, cities, or special tax districts on most types of real estate – including homes, businesses, and parcels of land. The amount of property tax owed depends on the appraised fair market value of the property, as determined by the property tax assessor.”

This organization also provides a map showing annual property taxes by state (including the District of Columbia), from lowest to highest, as a percentage of median home value. The top 5 states with the highest median property taxes are New Jersey, New Hampshire, Texas, Nebraska, and Wisconsin. The states with the lowest median property taxes are Louisiana, Hawaii, Alabama, and Delaware, followed by the District of Columbia.

The top 5 states with the highest median property taxes are New Jersey, New Hampshire, Texas, Nebraska, and Wisconsin. The states with the lowest median property taxes are Louisiana, Hawaii, Alabama, and Delaware, followed by the District of Columbia.

The top 5 states with the highest median property taxes are New Jersey, New Hampshire, Texas, Nebraska, and Wisconsin. The states with the lowest median property taxes are Louisiana, Hawaii, Alabama, and Delaware, followed by the District of Columbia.Bottom Line

Depending on where you live, property taxes can have a big impact on your monthly payment. To make sure your estimated taxes will fall within your desired budget, contact a local real estate professional today to find out how the neighborhood or area you choose can make a difference in your overall costs when buying a home.

Wednesday, September 25, 2019

Tuesday, September 24, 2019

Monday, September 23, 2019

Sunday, September 22, 2019

Friday, September 20, 2019

Monday, September 16, 2019

Sunday, September 15, 2019

Saturday, September 14, 2019

Friday, September 13, 2019

Thursday, September 12, 2019

Wednesday, September 11, 2019

Tuesday, September 10, 2019

Monday, September 9, 2019

Saturday, September 7, 2019

Friday, September 6, 2019

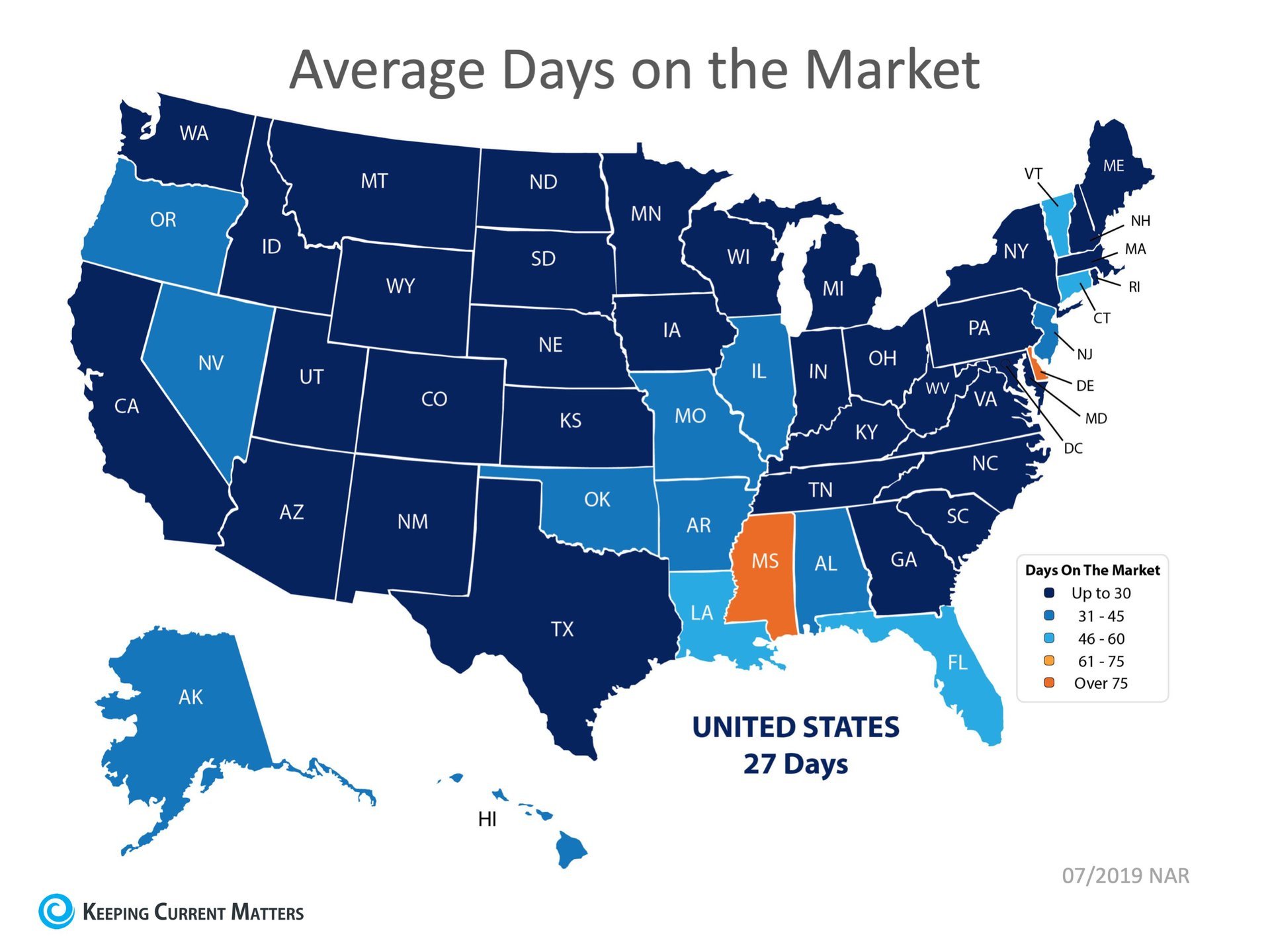

Why Now Is the Perfect Time to Sell Your House

As a homeowner, it’s always tempting to dream about the next big project you’re going to tackle. The possibilities are endless. Should I renovate? Should I refinance? Should I stay? Should I move? The list goes on and on.

As a homeowner, it’s always tempting to dream about the next big project you’re going to tackle. The possibilities are endless. Should I renovate? Should I refinance? Should I stay? Should I move? The list goes on and on.

In today’s housing market, it’s actually a great time to shift your thoughts toward selling your house and moving up into the home of your dreams. Here’s why:

Inventory is on the rise, but there’s still an overall shortage of houses for sale (less than a 6-month supply found in a more normal market), so homes are going under contract quickly. In fact, the National Association of Realtors (NAR) Realtors® Confidence Index Survey reports that right now homes are only staying on the market for an average of 27 days. That’s less than one month, an even more accelerated pace from the 36-day trend we saw last spring. The same report also indicates there are more interested buyers than active sellers today, which is one of the big factors driving home prices higher.

The same report also indicates there are more interested buyers than active sellers today, which is one of the big factors driving home prices higher.

This power combination provides an ideal environment for sellers aiming to close a quick sale and earn a big return as we wrap up the summer season.

This power combination provides an ideal environment for sellers aiming to close a quick sale and earn a big return as we wrap up the summer season.

The same report also indicates there are more interested buyers than active sellers today, which is one of the big factors driving home prices higher.This power combination provides an ideal environment for sellers aiming to close a quick sale and earn a big return as we wrap up the summer season.Bottom Line

There’s still time to make a move before the school year starts and the fall weather sets in. Maybe it’s time to make a change. Reach out to a local real estate professional in your area to determine if selling now is the right decision for your family.

Thursday, September 5, 2019

Tuesday, September 3, 2019

American Confidence in Housing at an All-Time High

Fannie Mae just released the July edition of their Home Purchase Sentiment Index (HPSI). The HPSI takes information regarding consumers’ confidence in the real estate market from Fannie Mae’s National Housing Survey and condenses it into a single number. Therefore, the HPSI reflects consumers’ current views and forward-looking expectations of housing market conditions.

Fannie Mae just released the July edition of their Home Purchase Sentiment Index (HPSI). The HPSI takes information regarding consumers’ confidence in the real estate market from Fannie Mae’s National Housing Survey and condenses it into a single number. Therefore, the HPSI reflects consumers’ current views and forward-looking expectations of housing market conditions.

Great News! The index reached its highest level since Fannie Mae began their survey. Breaking it down, the report revealed:

- The share of Americans who say it is a good time to buy a home increased from the same time last year.

- The share of those who say it is a good time to sell a home increased from the same time last year.

- The share of Americans who say they are not concerned about losing their job over the next 12 months increased dramatically (16 percentage points) from the same time last year.

- The share of Americans who say mortgage rates will go down over the next 12 months increased dramatically (24 percentage points) from the same time last year.

The day after the index was released, Freddie Mac also announced the 30-year fixed-rate mortgage rate fell to its lowest level in three years.

Doug Duncan, Senior Vice President and Chief Economist at Fannie Mae explained the uptick in the index:

“Consumer job confidence and favorable mortgage rate expectations lifted the HPSI to a new survey high in July, despite ongoing housing supply and affordability challenges. Consumers appear to have shaken off a winter slump in sentiment amid strong income gains. Therefore, sentiment is positioned to take advantage of any supply that comes to market, particularly in the affordable category.”

Bottom Line

Consumers are feeling good about the real estate market. Since Americans are not worried about their jobs, see mortgage rates near an all-time low, and believe it is a good time to buy, the housing market will remain strong for the rest of the year.

Monday, September 2, 2019

Subscribe to:

Comments (Atom)