Recently released data from the National Association of Realtors (NAR) suggests that a now is a great time to sell your home. The concept of ‘supply & demand’ reveals that the best price for an item is realized when the supply of that item is low and the demand for that item is high.

Let’s see how this applies to the current residential real estate market.

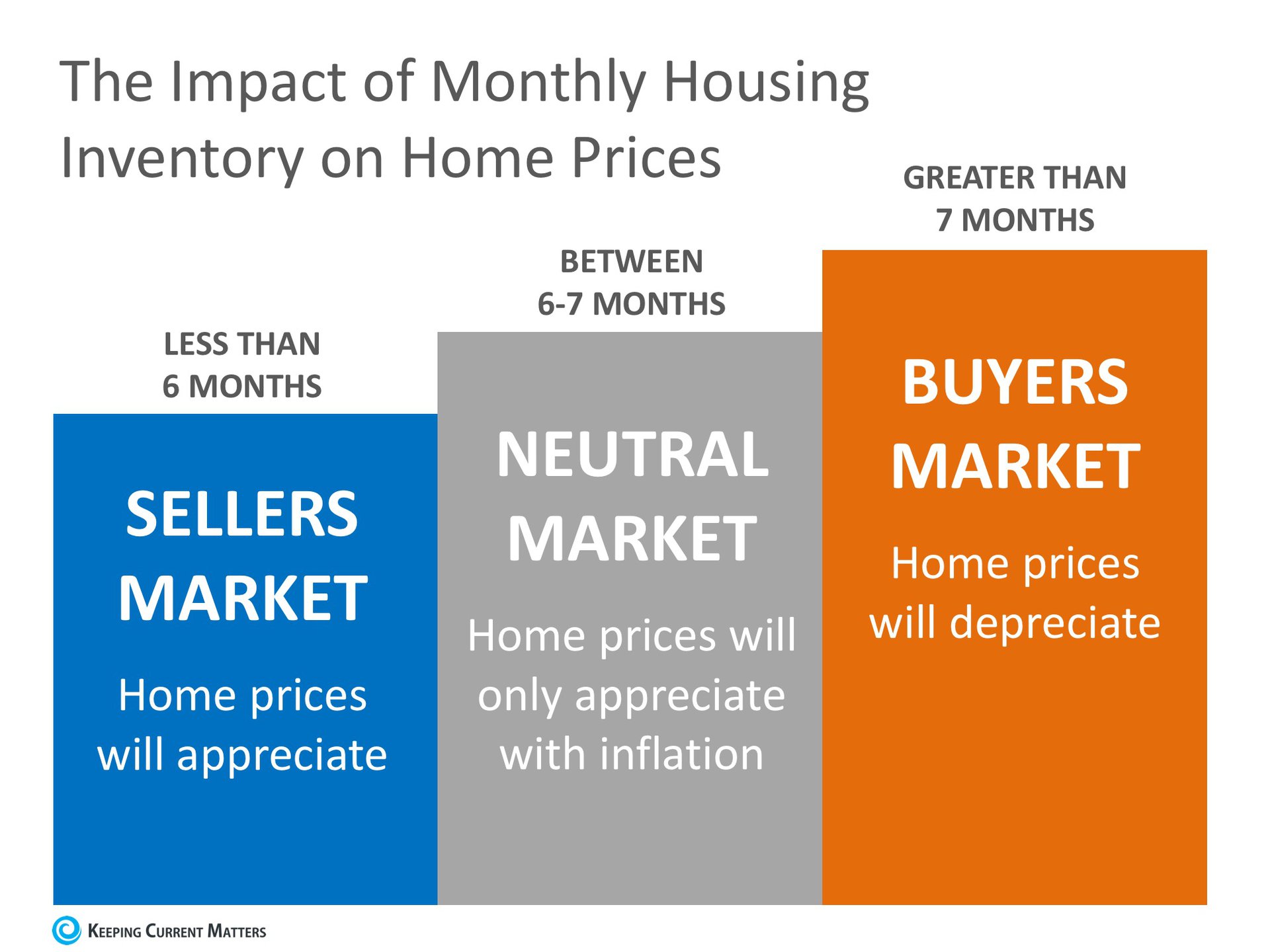

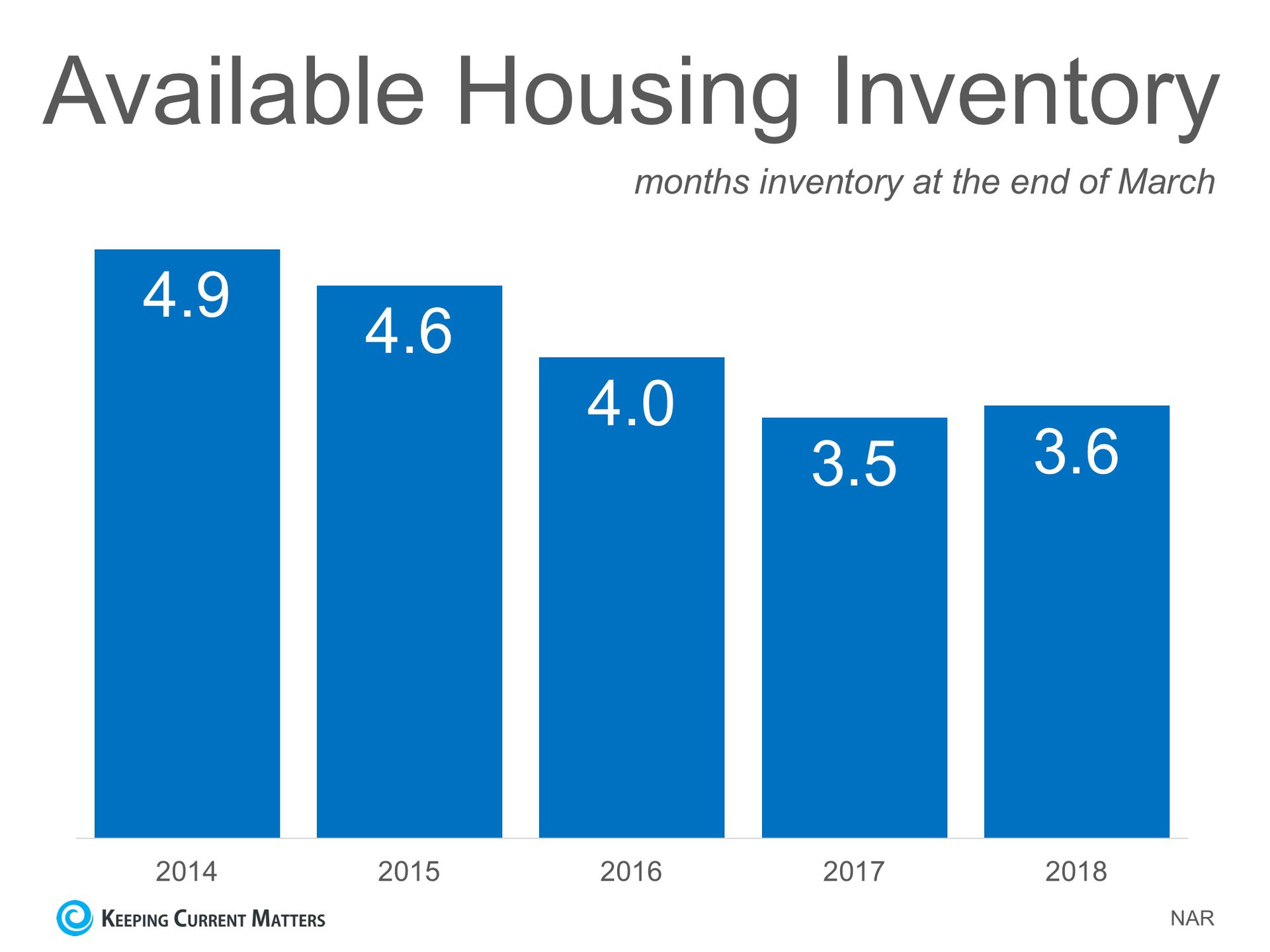

SUPPLY

It is no secret that the supply of homes for sale has been far below the number needed to sustain a normal market for over a year at this point. A normal market requires six months of housing inventory to meet the demand. The latest report from NAR revealed that there is currently only a 3.6-month supply of houses on the market.

Supply is currently very low!

DEMAND

A report that was just released tells us that demand is very strong. The most recent Foot Traffic Report (which sheds light on the number of buyers who are actually out looking at homes) disclosed that “foot traffic grew 10.5 points to 52.4 in March as the new season approaches.”

Demand is currently very high!

Bottom Line

Waiting to sell will only increase the competition between you and all of the other sellers putting their houses on the market later this summer. If you are debating whether or not to list your home, contact a local real estate professional who can explain the conditions in your market.

![3 Tips for Making Your Dream of Owning a Home a Reality [INFOGRAPHIC] | Keeping Current Matters](https://files.keepingcurrentmatters.com/wp-content/uploads/2018/05/08162959/3-Tips-KCM.jpg)

![50% of Homes Sold in 30 days in March [INFOGRAPHIC] | Keeping Current Matters](https://files.keepingcurrentmatters.com/wp-content/uploads/2018/05/01161030/20180504-Days-on-the-Market-KCM.jpg)

![Home Buying Myths Slayed [INFOGRAPHIC] | Keeping Current Matters](https://blogger.googleusercontent.com/img/proxy/AVvXsEhhFXmfB6bSUeHTiI3mLTD1bMmmCkH81rb-WgAE48T9vXnQ0A-0hNla53E_nD12mFqFjc5YEkVJeVc2VvkzGXi6gGP4zcqrAE976V-nUxhmwOX2YdGEYorErYnrZ9LE827kavKp2jBhuLG9CTqhv9iOGsPGUTeZ1vgHefnlndpCP5aIo1u7CskY2rOt93b9-IvhUoJQLBnSHMbAqg49_lVk=s0-d-e1-ft)

![Existing Home Sales Grow Despite Low Inventory [INFOGRAPHIC] | Keeping Current Matters](https://blogger.googleusercontent.com/img/proxy/AVvXsEirWL9xMRUKO0O2rAWQ4S2iJVHaa14Uealr8MXmmQu11Wgxx73cUjIcyGDpGrSfv-vEXlEfEJsb-bIa6Orx434Mfibjex8zSfl1NOCgD6Ha9RyKx7APJYvFch0gYPiwbIP_V4NyeQneNsuqfOWsZlrOJjqsVaYIAB7VeY-OIY6iSdN78njEhgBEhYm85YzM7MfMQTWwpAdhw498SNRydAvpOmrDFG2JjREB4_U=s0-d-e1-ft)