Every homeowner wants to make sure they get the best price when selling their home. But how do you guarantee that you receive maximum value for your house? Here are two keys to ensuring you get the highest price possible. Every homeowner wants to make sure they get the best price when selling their home. But how do you guarantee that you receive maximum value for your house? Here are two keys to ensuring you get the highest price possible.

1. Price it a LITTLE LOW

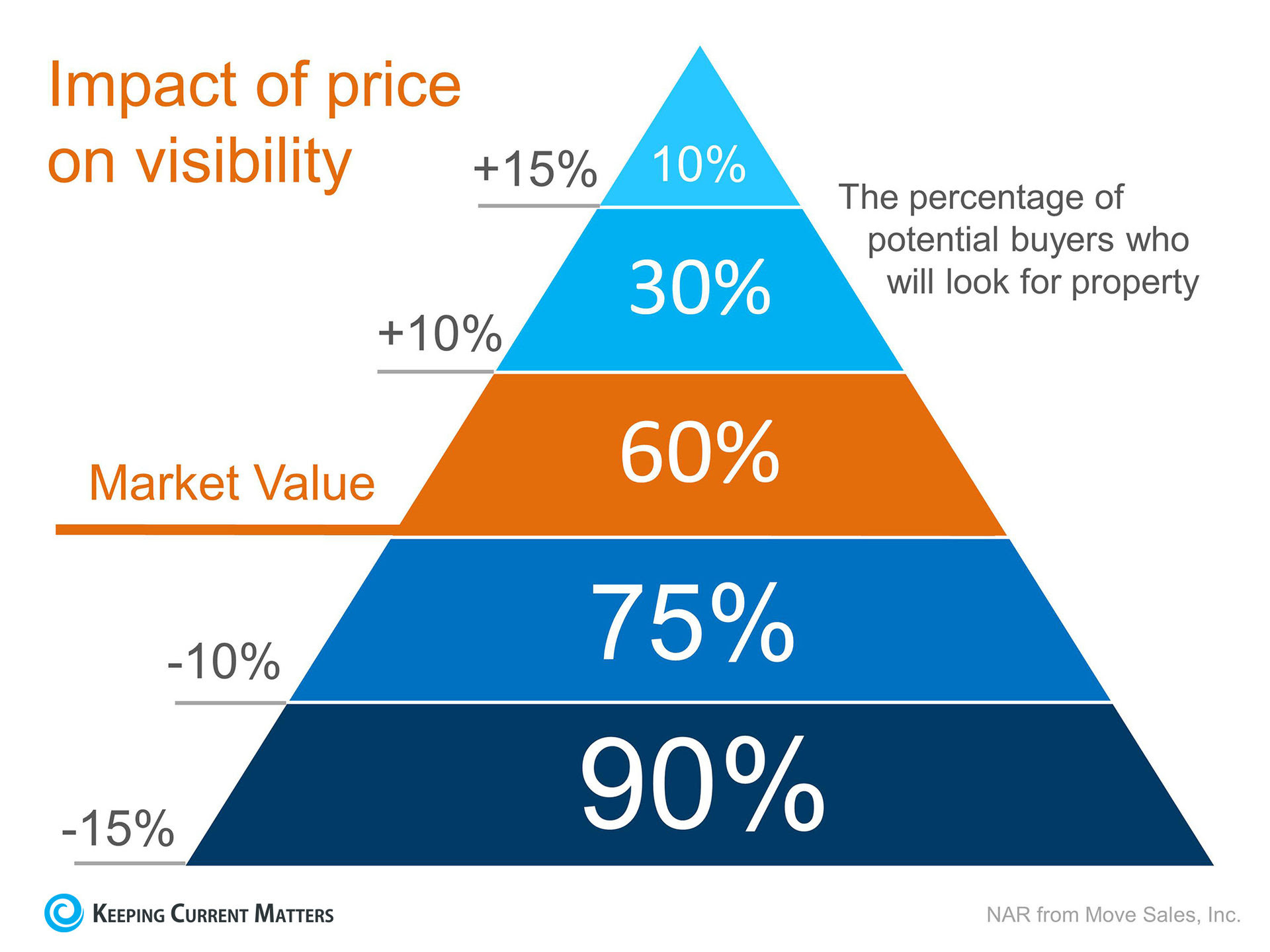

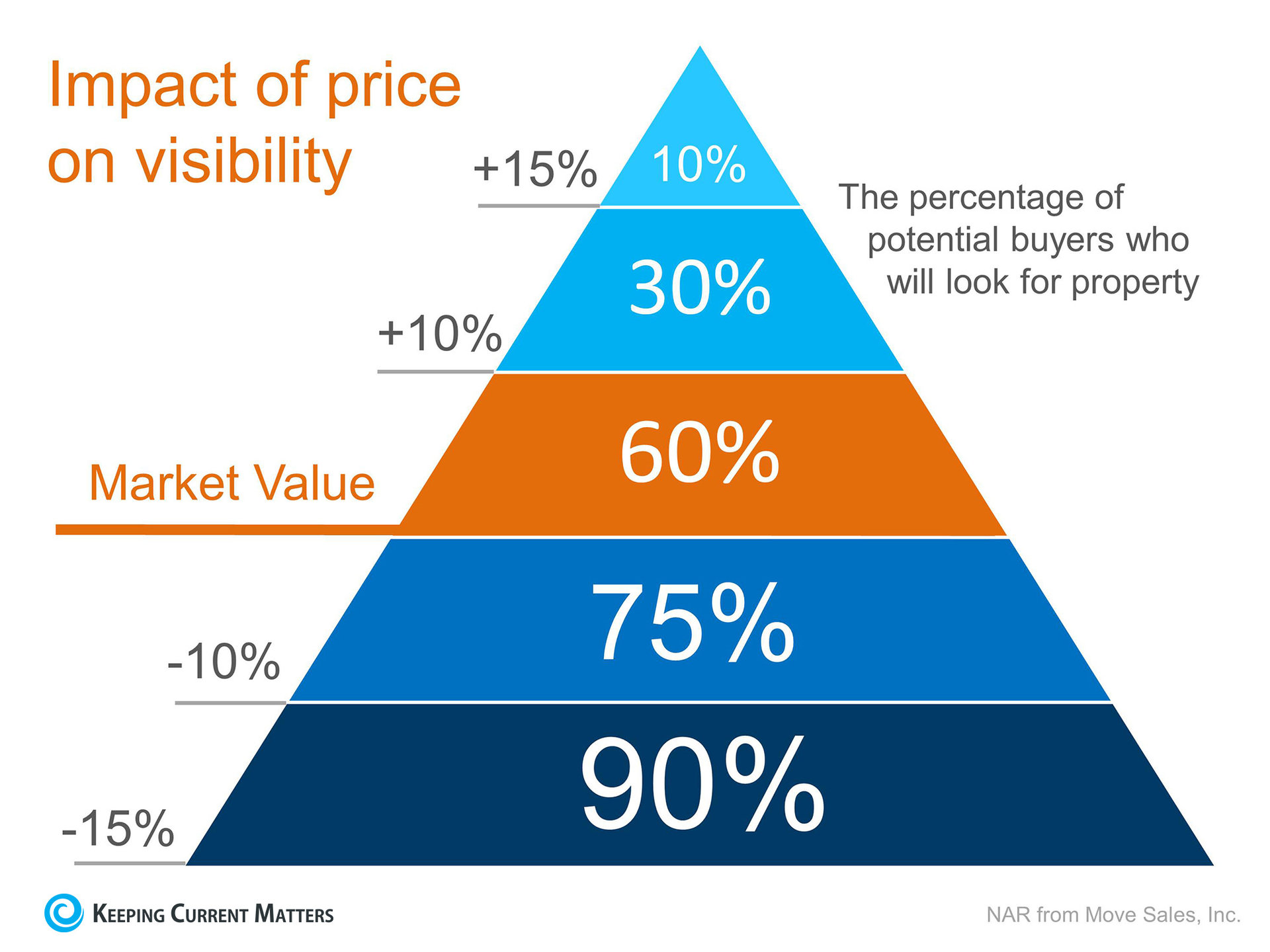

This may seem counterintuitive. However, let's look at this concept for a moment. Many homeowners think that pricing their home a little OVER market value will leave them room for negotiation. In actuality, this just dramatically lessens the demand for your house (see chart below).  Instead of the seller trying to 'win' the negotiation with one buyer, they should price it so that demand for the home is maximized. By doing this, the seller will not be fighting with a buyer over the price, but will instead have multiple buyers fighting with each other over the house. Realtor.com, gives this advice: Instead of the seller trying to 'win' the negotiation with one buyer, they should price it so that demand for the home is maximized. By doing this, the seller will not be fighting with a buyer over the price, but will instead have multiple buyers fighting with each other over the house. Realtor.com, gives this advice:

"Aim to price your property at or just slightly below the going rate. Today's buyers are highly informed, so if they sense they're getting a deal, they're likely to bid up a property that's slightly underpriced, especially in areas with low inventory."

2. Use a Real Estate Professional

This too may seem counterintuitive. The seller may think they would net more money if they didn't have to pay a real estate commission. With that being said, studies have shown that homes typically sell for more money when handled by a real estate professional. Research posted by the National Association of Realtors revealed that:

"The median selling price for all FSBO homes was $185,000 last year. When the buyer knew the seller in FSBO sales, the number sinks to the median selling price of $163,800. However, homes that were sold with the assistance of an agent had a median selling price of $245,000 - nearly $60,000 more for the typical home sale."

Bottom Line

Price your house at or slightly below the current market value and hire a professional. That will guarantee you maximize the price you get for your house. |

In today's market, with home prices rising and a lack of inventory, some homeowners may consider trying to sell their home on their own, known in the industry as a For Sale by Owner (FSBO). There are several reasons why this might not be a good idea for the vast majority of sellers. Here are the top five reasons:

In today's market, with home prices rising and a lack of inventory, some homeowners may consider trying to sell their home on their own, known in the industry as a For Sale by Owner (FSBO). There are several reasons why this might not be a good idea for the vast majority of sellers. Here are the top five reasons:

According to a

According to a

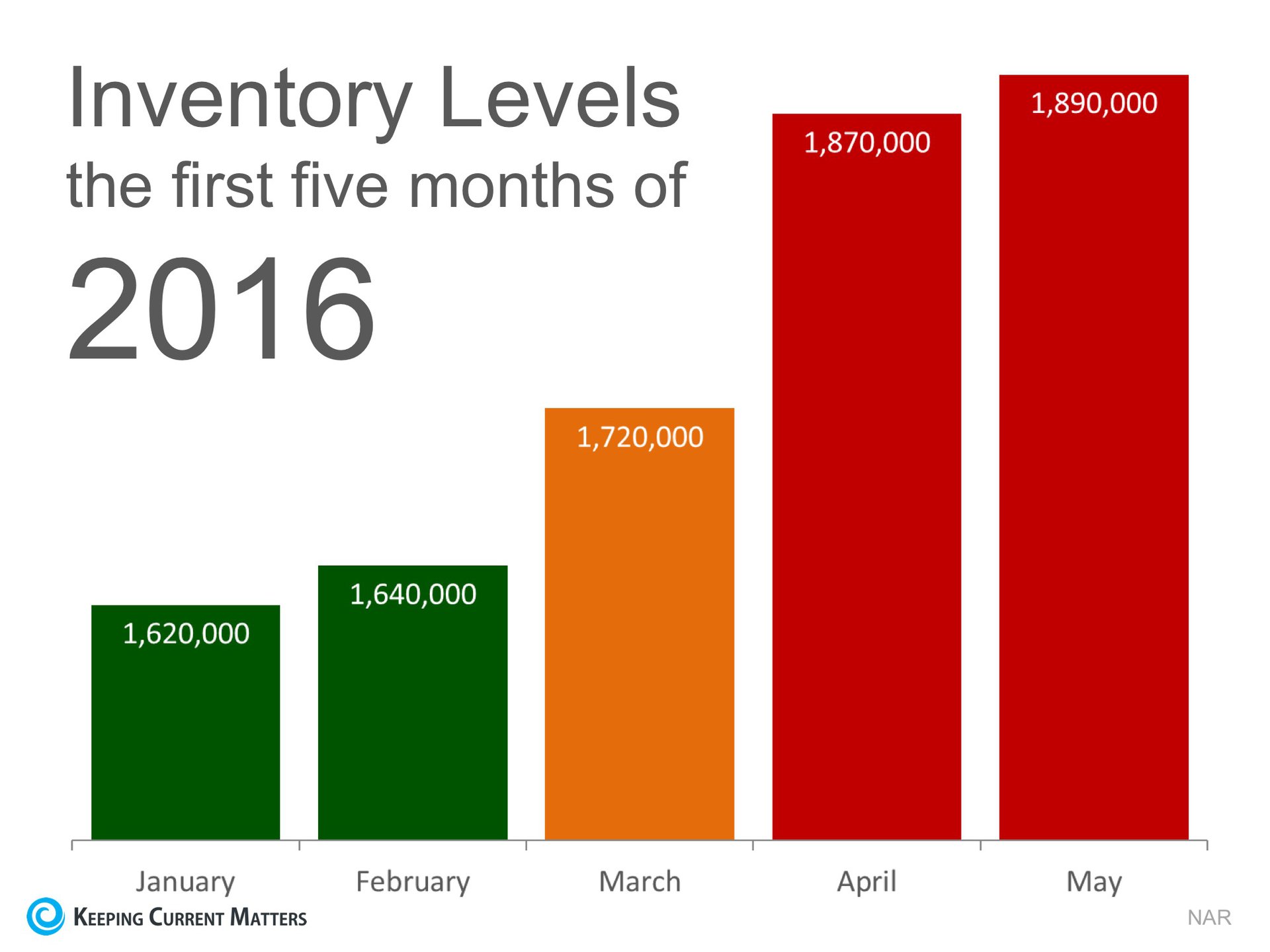

The price of any item (including residential real estate) is determined by 'supply and demand'. If many people are looking to buy an item and the supply of that item is limited, the price of that item increases. According to the National Association of Realtors (NAR), the supply of homes for sale dramatically increases every spring. As an example, here is what happened to housing inventory at the beginning of 2016:

The price of any item (including residential real estate) is determined by 'supply and demand'. If many people are looking to buy an item and the supply of that item is limited, the price of that item increases. According to the National Association of Realtors (NAR), the supply of homes for sale dramatically increases every spring. As an example, here is what happened to housing inventory at the beginning of 2016:

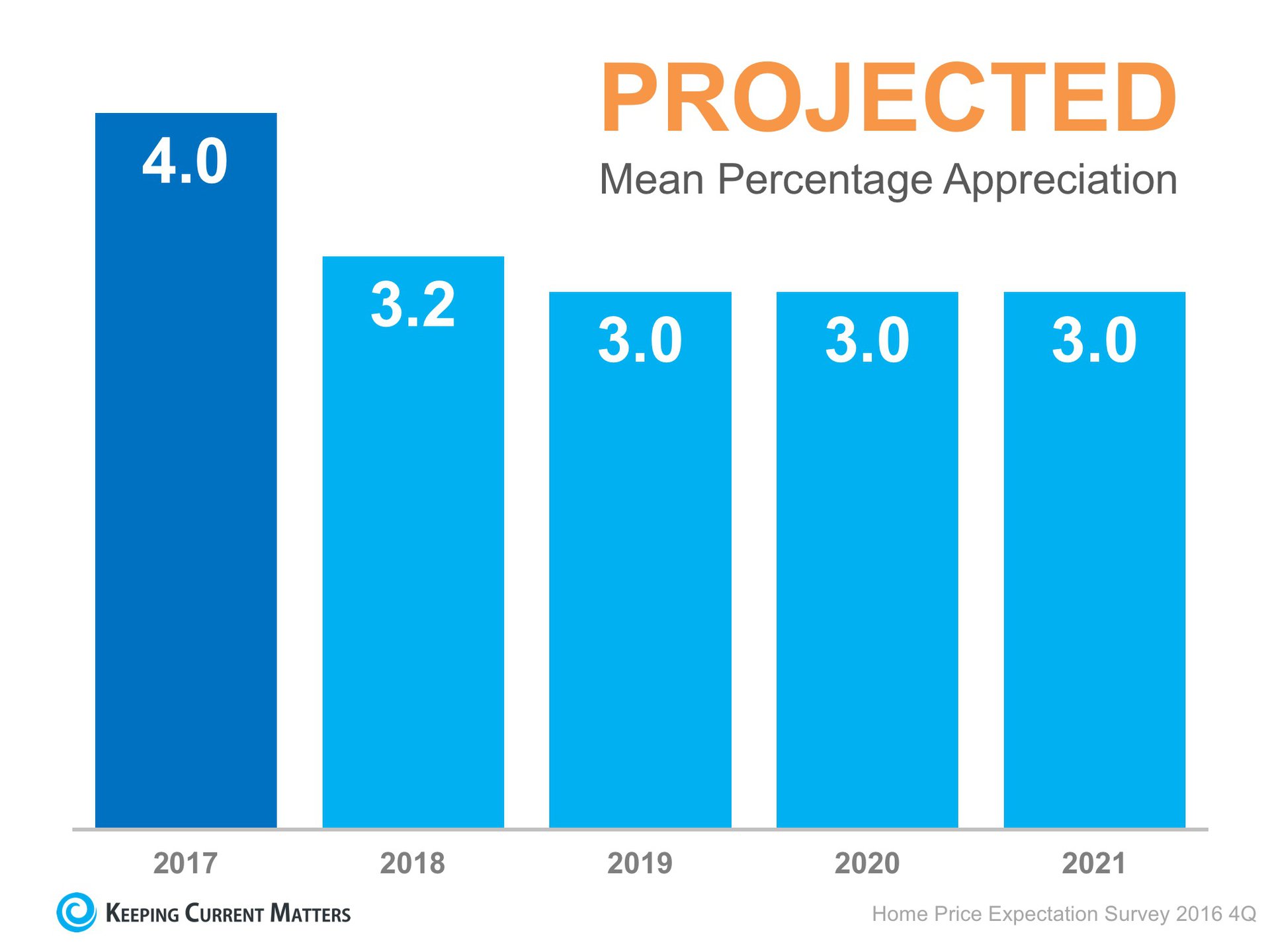

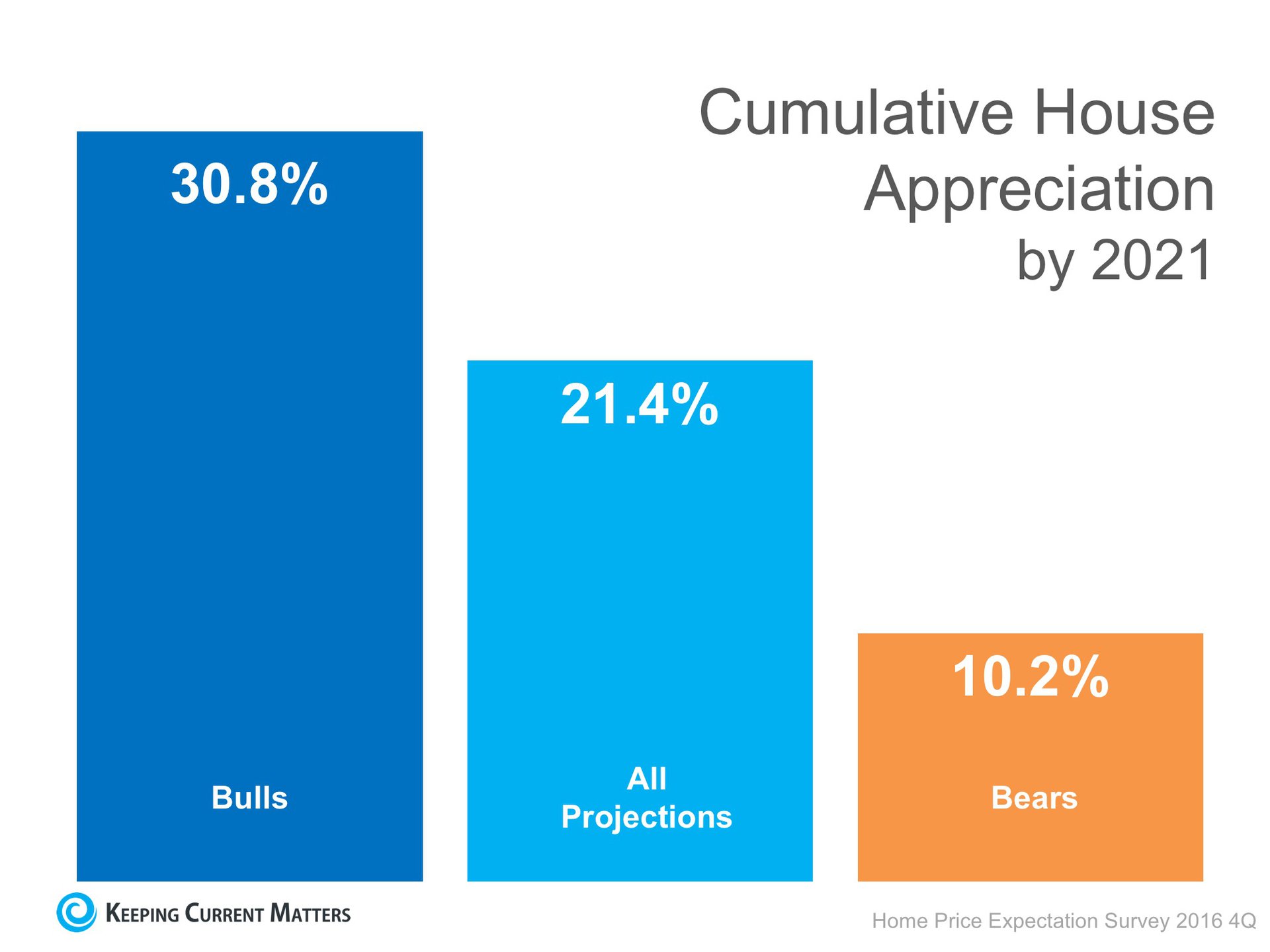

Over the next five years, home prices are expected to appreciate 3.24% per year on average and to grow by 21.4% cumulatively, according to Pulsenomics' most recent

Over the next five years, home prices are expected to appreciate 3.24% per year on average and to grow by 21.4% cumulatively, according to Pulsenomics' most recent

As the temperature in many areas of the country starts to cool down, you might think that the housing market will do the same. This couldn't be further from the truth! Here are 4 reasons you should consider buying your dream home this winter instead of waiting for spring!

As the temperature in many areas of the country starts to cool down, you might think that the housing market will do the same. This couldn't be further from the truth! Here are 4 reasons you should consider buying your dream home this winter instead of waiting for spring!

There is no doubt that mortgage credit availability is expanding, meaning it is easier to finance a home today than it was last year. However, the mortgage market is still much tighter than it was prior to the housing boom and bust experienced between 2003 - 2006. The Housing Financing Policy Center at the Urban Institute just

There is no doubt that mortgage credit availability is expanding, meaning it is easier to finance a home today than it was last year. However, the mortgage market is still much tighter than it was prior to the housing boom and bust experienced between 2003 - 2006. The Housing Financing Policy Center at the Urban Institute just

![New Home Sales Race to Keep Up with Demand [INFOGRAPHIC] | Keeping Current Matters](https://blogger.googleusercontent.com/img/proxy/AVvXsEjz-FU-27wNhyYcf_rp2LMsVEO8KqJewwzM_T804OwmPjiwnCMnj746BiqRdJsKdx5F05fv7twl2giNUVu2mV3gPKkhwwiswlZwpRuJ1TVNHOQn-iLOWIfnc-Sn11OIjNgXBCieoa5_mDsZyGDnLl6Q-7I3Fur-2kyejJIy1hx0E0yb45Hbjj5FvafQyLVRq5rQwMKkP3wHzA=s0-d-e1-ft)