Wednesday, November 30, 2016

Tuesday, November 29, 2016

Mortgage Interest Rates Just Went Up... Should I Wait to Buy?

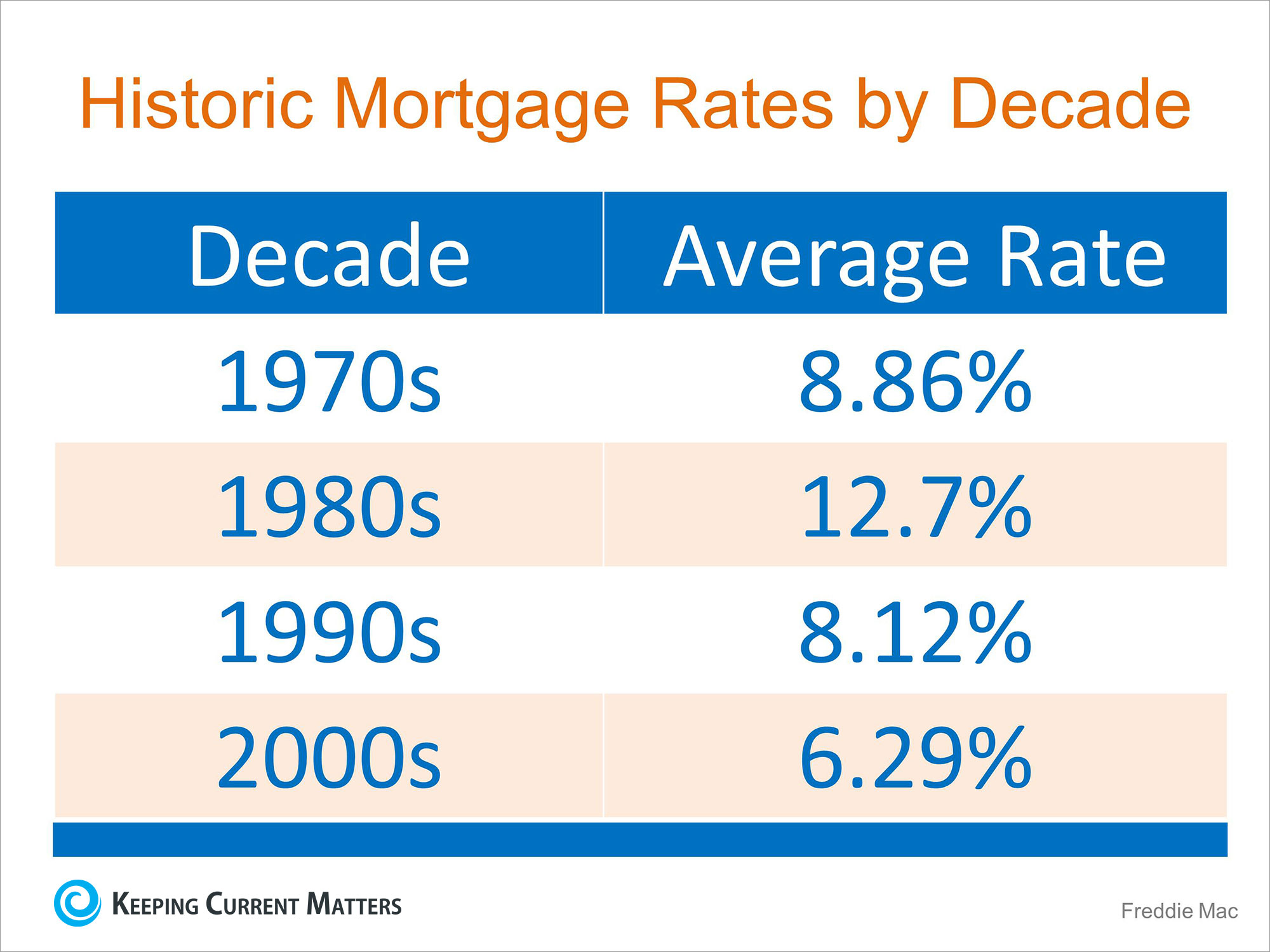

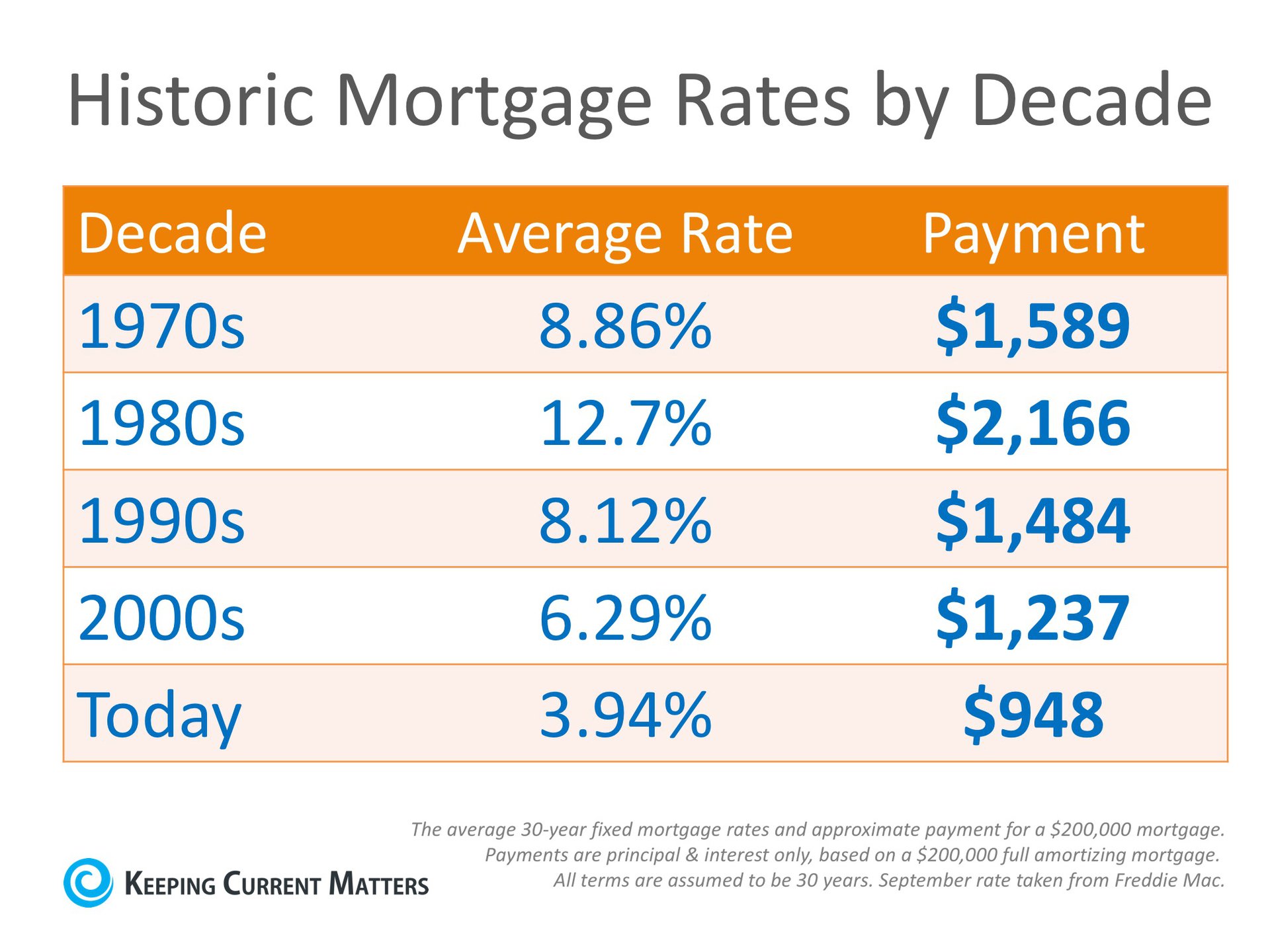

Mortgage interest rates, as reported by Freddie Mac, have increased over the last several weeks. Along with Freddie Mac, Fannie Mae, the Mortgage Bankers Association and the National Association of Realtors are all calling for mortgage rates to continue to rise over the next four quarters. This has caused some purchasers to lament the fact they may no longer be able to get a rate less than 4%. However, we must realize that current rates are still at historic lows. Here is a chart showing the average mortgage interest rate over the last several decades.

Mortgage interest rates, as reported by Freddie Mac, have increased over the last several weeks. Along with Freddie Mac, Fannie Mae, the Mortgage Bankers Association and the National Association of Realtors are all calling for mortgage rates to continue to rise over the next four quarters. This has caused some purchasers to lament the fact they may no longer be able to get a rate less than 4%. However, we must realize that current rates are still at historic lows. Here is a chart showing the average mortgage interest rate over the last several decades.

Bottom Line

Though you may have missed getting the lowest mortgage rate ever offered, you can still get a better interest rate than your older brother or sister did ten years ago; a lower rate than your parents did twenty years ago and a better rate than your grandparents did forty years ago.Monday, November 28, 2016

The Dangers of "Tight Mortgage Credit" Headlines

The availability of mortgage credit is not at the same level that it was during the boom in housing (2005), and that's good news. However, the constant headlines which talk about "tight credit" are causing some potential home buyers to doubt their ability to purchase. We want to rectify the misconception of what is required for a down payment in order to purchase a home in today's market. Freddie Mac recently discussed the confusion many first-time homebuyers have about the down payment they need in order to buy:

The availability of mortgage credit is not at the same level that it was during the boom in housing (2005), and that's good news. However, the constant headlines which talk about "tight credit" are causing some potential home buyers to doubt their ability to purchase. We want to rectify the misconception of what is required for a down payment in order to purchase a home in today's market. Freddie Mac recently discussed the confusion many first-time homebuyers have about the down payment they need in order to buy:"Did you know that the average down payment among first-time homebuyers is 6% and it's 13-14% for repeat buyers...It's possible to put down even less. Many potential homebuyers think that only the FHA helps make mortgage loans with low down payments. Not true. Freddie Mac's Home Possible mortgage products let qualified homebuyers put down as little as 3%."Brenda Garcia Lemus of John Burns Real Estate Consulting reports that this is also the case with newly constructed homes:

"Our home-builder clients sell hundreds of homes every weekend to buyers with 5% down payments and below average credit scores. Yet, many middle-income households with average credit and access to a 5% down payment assume they cannot become homeowners because of the 'tight credit' headlines."

Bottom Line

Before you 'disqualify' yourself, check with a professional in your market to find out what is possible in mortgaging today.Friday, November 25, 2016

Thinking of Selling? Don't Overlook an Outdated Kitchen, Buyers Won't

If you are planning on listing your home for sale, make sure that you don't overlook the condition of your kitchen. A recent article on realtor.com listed "7 Signs Your Kitchen Is Way Overdue for a Renovation," in which they warned:

If you are planning on listing your home for sale, make sure that you don't overlook the condition of your kitchen. A recent article on realtor.com listed "7 Signs Your Kitchen Is Way Overdue for a Renovation," in which they warned:"Dated kitchens--just like bathrooms--are a major barrier for resale. Buyers want modern amenities and styling, and most aren't interested in renovating post-purchase."Kitchen remodels can be pricey, with many complete remodels costing $20,000 or more. But not every kitchen needs a full remodel. There are many smaller projects that will help buyers see themselves trying their favorite Pinterest recipe in your home! Here are a couple of project ideas that, if you're handy or know someone who is, could end up boosting your home's value without breaking the bank:

- Are the cabinets in good shape but need an update? A new coat of paint and some updated hardware will instantly freshen up the space and drastically change the feel of the room all for under $300.

- A new backsplash to match the freshly painted cabinets updates the space and adds some style while staying under $200, depending on the size of the room.

- If the kitchen seems dark, consider adding LED under cabinet lighting for around $40.

- If replacing the countertops in the kitchen isn't within your budget, consider using a top coat to cover the current countertops.

"Eighty-two percent of homeowners said their updated kitchen gave them a greater desire to be at home, and 95% were happy or satisfied with the result."

Bottom Line

Kitchens and bathrooms are often make or break for buyers when touring a home or searching through photo galleries online. Consult a local real estate professional who can help you identify which small projects could pay off big!Wednesday, November 23, 2016

A Lack of Listings Remains 'Huge' Challenge in the Market

The housing crisis is finally in the rearview mirror as the real estate market moves down the road to a complete recovery. Home values are up, home sales are up, and distressed sales (foreclosures & short sales) are at their lowest mark in over 8 years. This has been, and will continue to be, a great year for real estate. However, there is one thing that may cause the industry to tap the brakes: a lack of housing inventory. According to the National Association of Realtors (NAR), buyer traffic and demand continues to be the strongest it has been in years. The supply of homes for sale has not kept up with this demand and has driven prices up in many areas as buyers compete for their dream home. Traditionally, the winter months create a natural slowdown in the market. Jonathan Smoke, Chief Economist at realtor.com, points to low interest rates as one of the many reasons why buyers are still out in force looking for a home of their own.

The housing crisis is finally in the rearview mirror as the real estate market moves down the road to a complete recovery. Home values are up, home sales are up, and distressed sales (foreclosures & short sales) are at their lowest mark in over 8 years. This has been, and will continue to be, a great year for real estate. However, there is one thing that may cause the industry to tap the brakes: a lack of housing inventory. According to the National Association of Realtors (NAR), buyer traffic and demand continues to be the strongest it has been in years. The supply of homes for sale has not kept up with this demand and has driven prices up in many areas as buyers compete for their dream home. Traditionally, the winter months create a natural slowdown in the market. Jonathan Smoke, Chief Economist at realtor.com, points to low interest rates as one of the many reasons why buyers are still out in force looking for a home of their own."Overall, the fundamental trends we have been seeing all year remain solidly in place as we enter the traditionally slower sales season, and pent-up demand remains substantial as buyers seek to get a home under contract while rates remain so low."NAR's Chief Economist, Lawrence Yun, points out that the inventory shortage we are currently experiencing isn't a new challenge by any means:

"Inventory has been extremely tight all year and is unlikely to improve now that the seasonal decline in listings is about to kick in. Unfortunately, there won't be much relief from new home construction, which continues to be grossly inadequate in relation to demand."

Bottom Line

Healthy labor markets and job growth have created more and more buyers who are not just ready and willing to buy but are also able to. If you are debating whether or not to put your home on the market this year, now is the time to take advantage of the demand in the market.Why Are Mortgage Interest Rates Increasing?

According to Freddie Mac's latest Primary Mortgage Market Survey, the 30-year fixed rate mortgage interest rate jumped up to 3.94% last week. Interest rates had been hovering around 3.5% since June, and many are wondering why there has been such a significant increase so quickly. According to Freddie Mac's latest Primary Mortgage Market Survey, the 30-year fixed rate mortgage interest rate jumped up to 3.94% last week. Interest rates had been hovering around 3.5% since June, and many are wondering why there has been such a significant increase so quickly.Why did rates go up?Whenever there is a presidential election, there is uncertainty in the markets as to who will win. One way that this is noticeable is through the actions of investors. As we get closer to the first Tuesday of November, many investors pull their funds from the more volatile and less predictive stock market and instead, choose to invest in Treasury Bonds. When this happens, the interest rate on Treasury Bonds does not have to be as high to entice investors to buy them, so interest rates go down. Once the elections are over and a President has been elected, investors return to the stock market and other investments, leaving the Treasury to raise rates to make bonds more attractive again. Simply put, the better the economy, the higher interest rates will go. For a more detailed explanation of the many factors that contribute to whether interest rates go up or down, you can follow this link to Investopedia.The Good NewsEven though rates are closer to 4% than they have been in nearly 6 months, they are still slightly below where we started 2016, at 3.97%. The great news is that even at 4%, rates are still significantly lower than they have been over the last 4 decades, as you can see in the chart below. Any increase in interest rate will impact your monthly housing costs when you secure a mortgage to buy your home. A recent Wall Street Journal article points out that, "While still only roughly half the average over the past 45 years, according to Freddie Mac, the quick rise has lenders worried that home loans could become more expensive far sooner than anticipated." Tom Simons, a Senior Economist at Jefferies LLC, touched on another possible outcome for higher rates: Any increase in interest rate will impact your monthly housing costs when you secure a mortgage to buy your home. A recent Wall Street Journal article points out that, "While still only roughly half the average over the past 45 years, according to Freddie Mac, the quick rise has lenders worried that home loans could become more expensive far sooner than anticipated." Tom Simons, a Senior Economist at Jefferies LLC, touched on another possible outcome for higher rates:"First-time buyers look at the monthly total, at what they can afford, so if the mortgage is eaten up by a higher interest expense then there's less left over for price, for the principal. Buyers will be shopping in a lower price bracket; thus demand could shift a bit." Bottom LineInterest rates are impacted by many factors, and even though they have increased recently, rates would have to reach 9.1% for renting to be cheaper than buying. Rates haven't been that high since January of 1995, according to Freddie Mac. |

Monday, November 21, 2016

NAR Reports Show Now Is a Great Time to Sell!

We all realize that the best time to sell anything is when demand is high and the supply of that item is limited. The last two major reports issued by the National Association of Realtors (NAR) revealed information that suggests that now continues to be a great time to sell your house. Let's look at the data covered by the latest Pending Home Sales Report and Existing Home Sales Report.

We all realize that the best time to sell anything is when demand is high and the supply of that item is limited. The last two major reports issued by the National Association of Realtors (NAR) revealed information that suggests that now continues to be a great time to sell your house. Let's look at the data covered by the latest Pending Home Sales Report and Existing Home Sales Report.THE PENDING HOME SALES REPORT

The report announced that pending home sales (homes going into contract) are up 2.4% over last year, and have increased year-over-year now for 22 of the last 25 consecutive months. Lawrence Yun, NAR's Chief Economist, had this to say:"The one major predicament in the housing market is without a doubt the painfully low levels of housing inventory in much of the country. It's leading to home prices outpacing wages, properties selling a lot quicker than a year ago and the home search for many prospective buyers being highly competitive and drawn out because of a shortage of listings at affordable prices."Takeaway: Demand for housing will continue throughout the end of 2016 and into 2017. The seasonal slowdown often felt in the winter months did not occur last winter and shows no signs of returning this year.

THE EXISTING HOME SALES REPORT

The most important data point revealed in the report was not sales, but was instead the inventory of homes for sale (supply). The report explained:- Total housing inventory rose 1.5% to 2.04 million homes available for sale

- That represents a 4.5-month supply at the current sales pace

- Unsold inventory is 6.8% lower than a year ago, marking the 16th consecutive month with year-over-year declines

"Inventory has been extremely tight all year and is unlikely to improve now that the seasonal decline in listings is about to kick in. Unfortunately, there won't be much relief from new home construction, which continues to be grossly inadequate in relation to demand."In real estate, there is a guideline that often applies; when there is less than a 6-month supply of inventory available, we are in a seller's market and we will see appreciation. Between 6-7 months is a neutral market, where prices will increase at the rate of inflation. More than a 7-month supply means we are in a buyer's market and should expect depreciation in home values. As Yun notes, we are, and will remain, in a seller's market with prices still increasing unless more listings come to the market.

"There's hope the leap in sales to first-time buyers can stick through the rest of the year and into next spring. The market fundamentals -- primarily consistent job gains and affordable mortgage rates -- are there for the steady rise in first-timers needed to finally reverse the decline in the homeownership rate."Takeaway: Inventory of homes for sale is still well below the 6-month supply needed for a normal market. Prices will continue to rise if a 'sizable' supply does not enter the market.

Bottom Line

If you are going to sell, now may be the time to take advantage of the ready, willing, and able buyers that are still out looking for your houseThursday, November 17, 2016

Wednesday, November 16, 2016

Tuesday, November 15, 2016

The Truth About Housing Affordability

From a purely economic perspective, this is one of the best times in American history to buy a home. Black Night Financial Servicesdiscusses this in their most recent Monthly Mortgage Monitor. Here are two of the report's revelations:

From a purely economic perspective, this is one of the best times in American history to buy a home. Black Night Financial Servicesdiscusses this in their most recent Monthly Mortgage Monitor. Here are two of the report's revelations:- The average U.S. home value increased by $13,500 from last year, but low interest rates have kept the monthly principal & interest payment needed to purchase a median-priced home almost equal to one year ago.

- Home affordability still remains favorable compared to long-term historic norms.

"Even though the value of the average home in the U.S. increased by about $13,500 over the last year, thanks to declining interest rates it actually costs almost exactly the same in principal and interest each month to purchase as it did this time last year. Even taking into account the fact that affordability can vary - sometimes significantly - across the country based upon the different rates of home price appreciation we're seeing, that's a pretty incredible balancing act between interest rates and home prices at the national level... Right now, it takes 20 percent of the median monthly income to cover monthly payments on the median-priced home, which is well below historical norms." However, the report warns that affordability will be dramatically impacted by an increase in mortgage rates. "A half-point increase in interest rates would be equivalent to a $17,000 jump in the average home price, and bring that ratio to 21.5 percent. This increase is still below historical norms, but puts more pressure on homebuyers."

Bottom Line

If you are ready and willing to purchase a home of your own, find out if you're able to. Now is a great time to jump in.Friday, November 11, 2016

Buying a Home? 4 Demands to Make on Your Real Estate Agent

Are you thinking of buying a home? Are you dreading having to walk through strangers' houses? Are you concerned about getting the paperwork correct? Hiring a professional real estate agent can take away most of the challenges of buying. A great agent is always worth more than the commission they charge, just like a great doctor or great accountant. You want to deal with one of the best agents in your marketplace. To do this, you must be able to distinguish an average agent from a great one. Here are the top 4 demands to make of your real estate agent when buying a home:

Are you thinking of buying a home? Are you dreading having to walk through strangers' houses? Are you concerned about getting the paperwork correct? Hiring a professional real estate agent can take away most of the challenges of buying. A great agent is always worth more than the commission they charge, just like a great doctor or great accountant. You want to deal with one of the best agents in your marketplace. To do this, you must be able to distinguish an average agent from a great one. Here are the top 4 demands to make of your real estate agent when buying a home:1. Tell the Truth About the Price

When making an offer on the home you want to buy, make sure that your agent walks you through their plan for getting both the seller - and the bank - to accept that price. Too many agents will just take the offer that you suggest and then try to 'work' both you and the seller in the negotiating phase later. In a competitive market, you need an agent who is going to help you make the best 'initial offer' so that you stand out from the crowd. Every house in today's market must be sold twice - first to you and then to your bank. The second sale may be more difficult than the first. When prices are surging, it is difficult for appraisers to find adequate, comparable sales (similar houses in the neighborhood that closed recently) to defend the selling price when performing the appraisal for the bank. A red flag should be raised if your agent is not discussing this with you at the time of the original offer.2. Understand the Timetable with Which Your Family is Dealing

You will be moving your family into a new home. Whether the move revolves around the start of the new school year or a new job, you will be trying to put the move to a plan. This can be very emotionally draining. Demand from your agent an appreciation for the timetables you are setting. Your agent cannot pick the exact date of your move, but they should exert any influence they can to make it work.3. Remove as Many of the Challenges as Possible

It is imperative that your agent knows how to handle the challenges that will arise. An agent's ability to negotiate is critical in this market. Remember: If you have an agent who was weak negotiating with you on parts of the purchase offer, don't expect them to turn into a superhero when they are negotiating with the seller for you and your family.4. Find the Right HOUSE!

There is a reason you are putting yourself and your family through the process of moving. You are moving on with your life in some way. The reason is important or you wouldn't be dealing with the headaches and challenges that come along with buying. Do not allow your agent to forget these motivations. Make sure that they don't worry about your feelings more than they worry about your family; if they discover something needs to be done in order to attain your goal, insist that they have the courage to inform you.Good agents know how to deliver good news. Great agents know how to deliver tough news. In today's market, YOU NEED A GREAT AGENT!

Wednesday, November 9, 2016

How Long Do Families Stay in a Home?

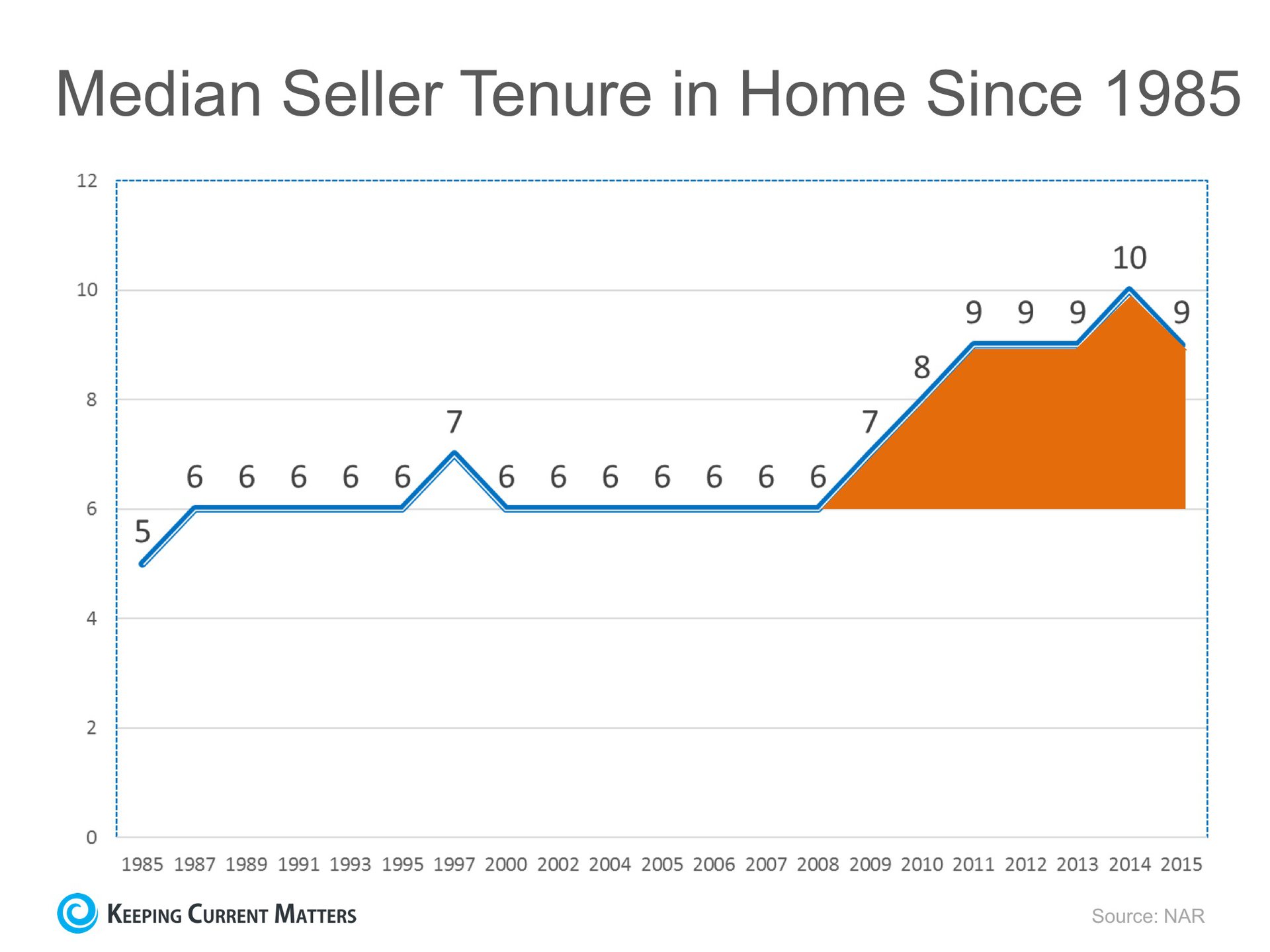

The National Association of Realtors (NAR) keeps historic data on many aspects of homeownership. One of the data points that has changed dramatically is the median tenure of a family in a home. As the graph below shows, for over twenty years (1985-2008), the median tenure averaged exactly six years. However, since 2008, that average is almost nine years - an increase of almost 50%. The National Association of Realtors (NAR) keeps historic data on many aspects of homeownership. One of the data points that has changed dramatically is the median tenure of a family in a home. As the graph below shows, for over twenty years (1985-2008), the median tenure averaged exactly six years. However, since 2008, that average is almost nine years - an increase of almost 50%.  Why the dramatic increase?The reasons for this change are plentiful. The top two reasons are:

What does this mean for housing?Many believe that a large portion of homeowners are not in a house that is best for their current family circumstances. They could be baby boomers living in an empty, four-bedroom colonial, or a millennial couple planning to start a family that currently lives in a one-bedroom condo. These homeowners are ready to make a move. Since the lack of housing inventory is a major challenge in the current housing market, this could be great news. |

Monday, November 7, 2016

Are Millennials Taking Over The Housing Market?

Millennials haven’t taken over the housing market yet, but it’s only a matter of time before they do.

Many Millennials have not moved into homeownership due to a number of factors, including a preference for urban living and a high student debt burden.

However, now first First American created a chart that shows Millennials have a higher percentage of people with a college degree than any other generation.

(Source: First American)

This educational advantage bodes well for future homeownership rates among this generation. A study from Fannie Mae showed that the long-term benefit of a college degree outweighs the short-term burden of student loan debt when it comes to the likelihood of eventual homeownership.

The study showed that those who earned a degree without taking on student debt are the most likely to become homeowners, followed by those who graduated with debt, those who never went to college and lastly, those who took on student debt but never graduated.

So Millennials' status as not only the largest demographic but also the most educatedgeneration ever could soon lead to abnormally high homeownership rates. That could come with a downside, however.

“The risk will be that prices will adjust to all of the demand and reduce affordability, making it more difficult,” First American Financial Corp. Chief Economist Mark Fleming told HousingWire.

“That’s why the issue of lack of inventory, whether in the form of less existing home sales than expected or a lack of right-priced new homes, is so important to the future success of the market to serve the possible tsunami of demand,” Fleming said.

Freddie Mac also thinks an influx in Millennial buyers is likely, and there is evidence this could already be starting. Existing home sales increased in September, driven mainly by a dramatic increase in first-time homebuyers, which reached the highest share of homebuyers in four years, according to a report from the National Association of Realtors.

Saturday, November 5, 2016

The Difference An Hour Makes

![The Difference an Hour Makes This Fall [INFOGRAPHIC] | Keeping Current Matters](http://www.keepingcurrentmatters.com/wp-content/uploads/2016/10/20161104-ENG-KCM-1.jpg)

Every Hour in the US Housing Market:

- 633 Homes Sell

- 253 Homes Regain Positive Equity

- Median Home Values Go Up $1.43

Subscribe to:

Comments (Atom)